Lessons From Loser Investments

Lessons From Loser Investments

You’ve Got Know When to Hold ‘Em, Know When to Fold ‘Em

The 10% rise in the S&P 500 index year-to-date is a headline that masks a lot of carnage which lies beneath the surface. If you took away a handful of stocks – Apple (AAPL), Alphabet (GOOGL), Amazon (AMZN), Meta Platforms (META), Microsoft (MSFT), Nvidia (NVDA), and Tesla (TSLA), the so-called “magnificent seven” – the market would barely be up at all.

Things have been particularly rough in small cap land, thanks to the 16% drop in the Russell 2000 index since its high on July 31.

After this much volatility, almost every investor I know – especially ones who are active in small caps – is sitting on some unrealized losses. While the inclination in these situations is often to play a masochistic game of “Shoulda, Coulda, Woulda”, the more productive path forward is to do a thorough review of the losers and make a plan of action, which rarely means sitting still and licking your wounds.

You Buy Your Portfolio Everyday

It’s a trite phrase, but it is also an accurate one. Every dollar you have tied up in an investment has an opportunity cost of not being tied up in a better investment. Holding a loser stock so you can someday “make it back to even” is a psychological game that almost everyone is inclined to play but is rarely a good strategy.

Does that mean I am telling you that you should sell ALL your losers? Absolutely not.

That might be the advice that a more momentum-driven investor would give you. But that’s not me. As a fundamental investor with a value tilt, I strongly believe that stocks often overshoot to the downside. Markets aren’t always efficient.

Dislocations in the overall market, certain sectors within the market, or individual stocks can be great - albeit stressful - money-making opportunities. It’s another trite phrase – but I truly believe fortunes are made in bear markets and collected in bull markets.

Folding

It’s much more fun to tell you about the investments that worked, but show me an investor who has no losers, and I’ll show you a liar. We all have them, it’s part of the game. But how you deal with losers will make a big difference in your overall long-term returns.

One stock I recently took my lumps on is athletic footwear retailer Foot Locker (FL). It was a particularly painful loss, because early in my holding period, I made a quick double-digit gain on the stock… but only on paper.

When I bought FL shares, the stock was in the $40s and extremely cheap on earnings per share (“EPS”) of over $7, trading at a price to earnings ratio (“P/E”) of just 6-7 times. I knew that the company was at peak earnings at that point, and I thought EPS could drop to $4 to $5, which would have put the stock at a still attractive less than 10 P/E on “normalized earnings.”

Earnings turned out to have more downside than I expected…. In March, management dropped 2023 EPS guidance to around $3.50. I nevertheless stuck with the stock when it fell under $30, partly because I thought that guidance cut would be the only one. A lot of my patience with the stock hinged on my faith in the new CEO, Mary Dillon, who had been tremendously successful in her long tenure at cosmetics retailer Ulta Beauty (ULTA).

Well, macro headwinds, increased competition, and reduced allocations from key supplier Nike (NKE) led to two more cuts to 2023 guidance, and now Foot Locker is expected to only make around $1.40. My thesis that relations between Nike and Foot Locker were stabilizing and that sneaker demand would be relatively resilient was completely wrong. My original thesis was clearly already breaking in the spring, but I ignored that, because I came up with a new thesis that revolved around the CEO.

If retail legend Mary Dillon would take this job, there clearly had to be something compelling about Foot Locker, right? She had plenty of money already since ULTA shares had risen about 250% during her eight-year tenure as CEO… why would she go to Foot Locker if she didn’t see tremendous potential there? This line of logic had worked for me before – notably when extremely successful former Foot Locker CEO Ken Hicks had come out of retirement to lead Academy Sports & Outdoors (ASO) in the years preceding and following its 2020 initial public offering (“IPO”). ASO shares have performed tremendously. But this time, the logic didn’t work.

My sin here was thesis drift. I bought a stock for one reason, and when it didn’t work out, I found another reason to keep holding on. Both theses seem broken at the moment. So I sold the stock, and redeployed funds into other stocks that got caught in the consumer sector downdrift. For my sin of thesis drift, I paid the hefty price of losing about 50% of my money, when I could have kept it closer to a 30% loss had I sold on that first negative earnings revision.

I probably made a bad sale. I have no doubt that someday, FL shares will trade materially higher than where I sold them. But I freed up that money to buy stocks that I think can either go up more than FL shares will or go up the same amount but sooner/faster.

Holding

I bought a few stocks with the money I freed up from selling Foot Locker and other losers. There were a few new positions initiated, but the stock I am going to talk about here is the giant loser I added to. Because when a stock you own is down a lot, if you aren’t going to sell it… you should probably be buying it. Because it is on sale! If you loved it at $100, you must really love it at $60!

I presented this “loser stock” at the Cyprus Value Investor Conference in September, and I began with something like “if you like stocks that go down every day… do I have the idea for you!” And I was only half-kidding. Because this stock has been a dog… no pun intended – it’s pet goods retailers Petco Health and Wellness (WOOF). As if the price performance isn’t bad enough, it’s a broken IPO with a vanity ticker. Consider yourself warned!

At the end of this piece, I am going to share my slide deck on Petco so you can dig into all the details of how I am thinking about it. But I’ll go through the highlights of my investment thesis here.

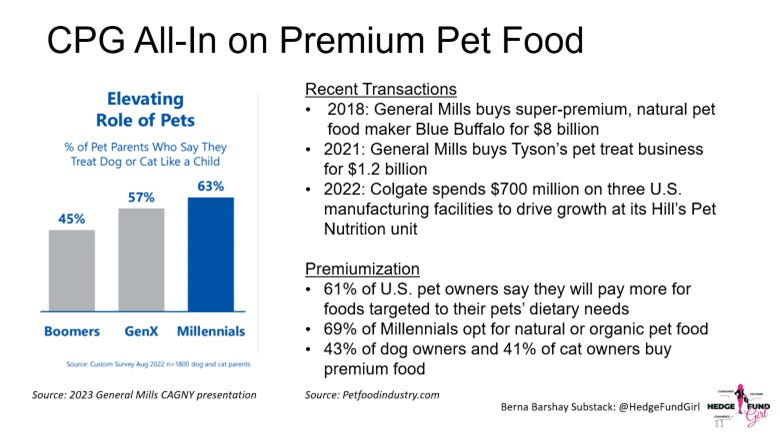

At the highest level, I think Petco is a good business going through a rough patch. The pet business in general – encompassing both retail and healthcare – has been an attractive one for many years. Over time, pet ownership has grown and the amount of money that people spend on their pets has also grown. As pets get more and more humanized, treated like a member of the family and not a possession, people have been buying higher quality food, more toys and clothes and other accessories, and taking their animals to the vet more often, often opting for more preventative care. As a result, pet food and snacks has been one of the fastest growing areas of consumer-packaged goods (“CPG”) and there have been a ton of deals in the sector.

Petco itself was taken private not once – but twice – by private equity, and a few years ago it was sold from one private equity group to another. So three times in just over 20 years, there was someone out there willing to buy this whole business. This is an encouraging sign to me.

Unfortunately, this 1500-store omnichannel retailer is not immune to macroeconomic headwinds. Business has slowed down significantly, and some customers are trading down to cheaper foods.

Another big problem is its “COVID hangover.” Tons of people adopted new pets during the peak pandemic years of 2020 and 2021. The good news is those pets are on average going to live 10 to 15 years and need to be fed and cared for. The bad news is that many pet supplies like dog crates and cat trees are very high margin – and you only buy them once or twice during a pet’s life.

The gross margin on supplies and accessories can be 30 points higher than in consumables like food and litter. The shift back from start up type supply purchases to ongoing consumables purchases has been like a lead weight on Petco’s gross margin, which is down a couple hundred basis points from the pandemic peak. Comps will get easier, and over time, the supply business should get a little better as pet adoptions pick up or the replacement cycle for these goods kicks in, but it is going to take time.

While we’re waiting, there is also the headwind of the economy. To be clear – I don’t expect business to get much better at Petco in the short term. But with the stock down 62% this year and trading at around $3.50 and less than $2.4 billion in enterprise value for over $6 billion in annual sales, I think its current operating troubles are priced in.

I am basically making a bet that the trend of humanizing and pampering pets, leading to increased spending in the category, is a secular trend interrupted, but not erased. I believe in the durability of this trend, but I also believe the economy is derailing it at the moment, just like the pandemic derailed the long-term trend of consumers emphasizing experiential spending (travel, concerts, dining) over spending on goods. Experiential spending came roaring back once it was safe to get back out there, and once we are on the other side of inflation, rate hiking, and the consumer economic pressures they bring, I think spending on Fido and Fluffy comes back as well.

Beyond a macro-driven rebound, there are a couple of other things that I think Petco has going for it.

First, I think it has a durable competitive advantage in e-commerce based on its use of its 1500-store footprint for ship-from-store local delivery. Based on my conversations with people working in the pet goods industry both in brick & mortar and online, I think fulfillment using ship-from-store costs materially less than ship-from-distribution center.

Shipping big, heavy bags of food and litter that have thin gross margins is a pretty terrible business. I think pet food is probably a loss leader for Amazon, and pet e-tailer Chewy’s EBITDA (earnings before interest, taxes, depreciation, and amortization) margins, which hover around 2%, are further proof of the intuitive fact that it is hard to make money selling this stuff online.

Selling pet food online will never be a good business, but I think Petco has cracked the code to make it a marginally profitable one by utilizing ship-from-store. As for brick & mortar operations, Petco does a great job in a category that will always inspire some in-person trips because of immediate, unpredictable needs. It also strategically uses its services business, which offers grooming and training, to pull people into the store.

Second – speaking of services – Petco is building out a veterinary business. It has 268 vet hospitals – or “Vetcos” in its stores, with plans to expand to 1000 locations. While there is an investment period associated with these startup ventures as they build their local clientele, over time, the vet business should be highly accretive since its margin at maturity should be about twice that of the retail business.

The company appears to be on track to meet its goals for Vetco and has done a great job recruiting vets in a very tight labor market. Petco has a lot to offer young vets who want to practice medicine and not spend their time running a small business. Petco’s flexibility around hours and job sharing has also made it attractive to young female vets balancing work and family responsibilities – and the majority of vet school grads now are women.

Private equity has been really active in the vet hospital space, and it’s not a stretch to imagine that based on comparable transactions, the “Vetco” business could be worth $1 billion now, based on the current number of facilities and run rate revenue.

There’s a lot I like about Petco, but one thing I don’t like is that I can’t totally explain why it has gone down so much. Since the beginning of the year, expectations for EBITDA are down 23%. But the stock is down 62%!

My best guess on why the stock has been so terrible is that its financial leverage has investors spooked. The company went public (again) in 2021 at $18, and still has leverage of over 3x EBITDA, thanks to its history as a private equity-sponsored leveraged buyout. Interest rates have exploded upward, and the debt is only 2/3 hedged. That said, this company has time… its only debt is a term loan that doesn’t expire until 2028. There’s a long time between now and then, and there is wiggle room for the business to get worse before it gets better without throwing the business into bankruptcy.

That said, there is clearly an aversion right now to leveraged equities where business is already weak. And that’s probably why the stock is under $4 and trading at an enterprise value to sales ratio of just 37%, despite Petco having more in common with a grocery store than a volatile high fashion retailer.

But leverage cuts both ways. Not only can it lead to the kind of stock drop that WOOF shares have experienced when things go wrong, but when things go a little right, small changes in performance can lead to big gains.

In my base case, where things pretty much stay as they are but just don’t get worse, I can see more than 100% upside to the stock… and if there is some margin recovery, it’s not impossible to imagine this stock getting back to its IPO price in a few years, which if it happened would represent a 400% return. This is a bull case and not what I am predicting, but it doesn’t take insanely heroic assumptions to get there.

On the flip side, this is a retailer with a lot of debt and leases, where things are currently not going well. I don’t think people are going to abandon their pooches, but it’s totally possible that in a weak economy, consumers trade down and cut back, to the major detriment of Petco’s P&L.

If absolutely everything went wrong here – yes, Petco could go bankrupt. That is a down 100% scenario, but I think I would see the signs along the way and have a chance to get out down maybe 50%. 50% would be a big loss, but that’s a worst-case scenario, and my best-case scenario is up 400%.

Simply put, I gladly will risk 50 cents for the chance to make $4… that is a bet I want to take. That’s an asymmetric bet with 8 potential units of reward to 1 unit of risk, in the bull case. And in my more conservative base case, it’s still almost 3 units of potential reward to 1 unit of risk.

One of the reasons I sold Foot Locker was the ratio of possible reward to possible risk was more like 2 to 1, and I want to free up funds for the 8 to 1 bet. I had a very small position in Petco that I initiated at around $9 (ouch) but the position is about three times as large now that the stock has been cut in half (and then some).

I’ve shared three of my slides above – and there’s one more to come, but there are about another 20 of them. If you want to review the slides and learn more about how I am thinking about Petco, click here.

Beyond Petco – Some Broader Lessons

Even if you hate this Petco idea – what, you don’t like stocks that go down every day??? – there are a few concepts I hope you can take away from this analysis.

1. Think About Units of Reward to Units of Risk

Ask yourself: how much can I make versus how much can I lose? What is the return in my bull case versus my bear case? If the ratio isn’t at least 2 to 1, I don’t usually get involved in the stock. There are a lot of different ways to get to two to one. You could have a sleepy large cap compounder that you think can go up 20% but also is unlikely to drop more than 10%. Or you could be buying portfolio jet fuel where the stock is either going bankrupt or going to double overnight. In my experience, finding anything above a 3 to 1 reward to risk ratio is usually hard without considering relatively high-risk names.

2. Size Risky Names Accordingly

You typically don’t get a shot at doubling your money – or tripling it – in a few years without taking on a lot of risk. Only invest what you can afford to lose in inherently risky names like Petco. These high risk/high reward names can really propel your overall returns when they work, but even great investors will blow up on risky names often, with the bear case coming to fruition. I anchor my single stock investing with big names like some of the ones in the magnificent seven, and others outside the list, like Eli Lilly (LLY) and McDonalds (MCD). I don’t think any of these companies are likely to double from here in a short period – but the chances of them going bankrupt is also near zero. So I like to barbell my portfolio with “relatively safe” large caps at one end of the spectrum, and high octane, well-researched but risky bets like Petco at the other end of the spectrum. My position in a lottery ticket like Petco would only be a fraction of the size of a position in a company like Alphabet because Petco is SO MUCH RISKIER.

3. Thinking About Turnarounds

When considering a turnaround investment like Petco, it’s important that companies have the financial wherewithal to get through the tough times. Especially when carrying a lot of debt, time needs to be on their side, which is why that 2028 date for the bank loan expiration is key. Here’s a slide with some other questions to ask about retail turnarounds:

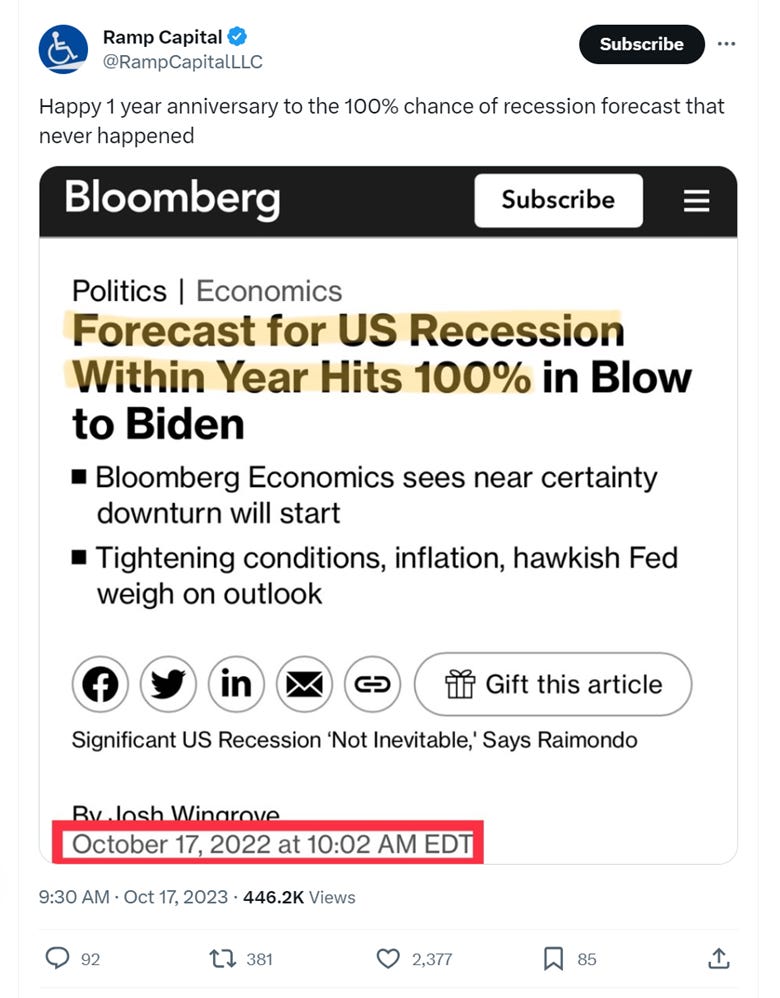

Tweet of the Week

This really cracked me up.

ICYMI, I previously addressed the permabears here.

A Quick Apology (or two)

I’m sorry it was so long in between posts. Late summer/early fall travels plus market volatility got in the way of my writing. Then when I finally got around to writing, there were a lot of built-up thoughts, so this is SO long!

I try to write when I really have something to say – not just for the sake of writing. But I also know that readers want some consistency. I am grappling with whether to produce deep dives versus quick, shorter hits on market topics or individual stocks. Would you rather hear from me more frequently, or do you prefer a more robust piece? Is once/month enough to hold your interest? Twice a month? Or do you want to hear from me weekly, even if it is just a curated reading list or a hot take on a company’s earnings? Is it important to you that I stick to a regular publishing schedule?

If you have thoughts, please let me know in the comments!

Some Interesting Things I Read Recently

Magnificent Seven tech stocks haven’t been this cheap in six years, Goldman Sachs strategists say

MarketWatch, 10/2/2023

More on the Magnificent Seven.

The Dial, 9/5/2023

The two biggest stories in the market this year are AI and GLP-1 drugs. Here’s the story of a blockbuster drug’s impact on a small country.

In TV’s Wild West, Which Channels Will be Dropped Next?

The Hollywood Reporter, 9/20/2023

If you still have cable, your channel line up is probably going to get downsized.

Prosperous Investing!

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice or a recommendation for a particular investment.

Disclosure: The author may have a personal financial interest in the securities mentioned. At the time of publication, personal investments included AAPL, GOOGL, LLY, MCD, META, and WOOF.

You are one of my favorites. To answer your questions: I don't care about a regular schedule and also not about a minimum number of pieces in a specific time period. I prefer to read from you

i) if you have conviction about an investment that you are familiar with from following it for a long time / thoroughly researched. 2 great ideas a year are better than 12 of which 10 are okish, because someone believed they have to submit something every month.

ii) if you have anything else to share that you think is interesting, e.g. you saw some earnings and you have some interesting thoughts about it because you followed the industry and specific companies for such a long time and your familiarity with them, that only few have.

I.e. less generic stuff, more of your in-depth industry applied to recent developments / opportunities.

Interesting write up on WOOF.

Do you think that [ship from store is cheaper than ship from DC] holds across different types of consumption? Eg are TGT/WMT structurally advantaged in their common SKU counts vs AMZN 1p/3p? Why haven’t grocery succeeded in 1p delivery?

Ie, is there some reason why ship-from-store will win in pet consumables despite not having obviously (yet?) won in books/toys/groceries/sundries?

Thanks again for sharing your thoughts!