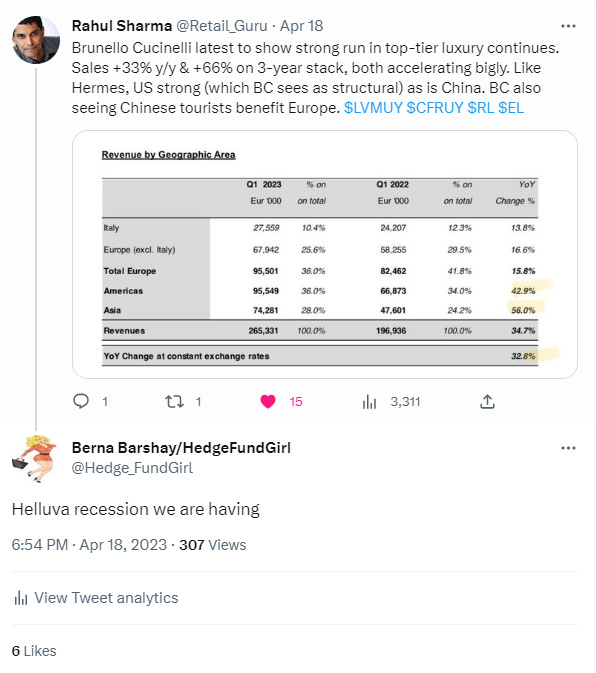

“Helluva recession we are having”

“Helluva recession we are having”

Despite plenty of mixed signals, the consumer is hanging in better than expected.

“Helluva a recession we are having.”

This was my reaction to a tweet calling out the exceptionally strong first quarter revenue growth posted by Italian luxury goods company Brunello Cucinelli (BC – Italy), best known for its beautiful – and pricey – cashmere creations.

(@Retail_Guru is a great account to follow on Twitter btw if you are interested in the consumer sector.)

But the strong results aren’t confined to just the luxury goods sector, which admittedly services primarily the global rich and global merely just very affluent.

We’re seeing some crazy numbers in travel too. Back in April, Delta Air Lines (DAL) reported total revenue per available seat mile (“TRASM”) up 16% versus 2019 and March quarter bookings that were 20% higher than in 2019, driven by strength in consumer leisure travel as well as the ongoing business travel recovery.

People are also spending to eat out. A few weeks ago, Chipotle Mexican Grill (CMG) reported comparable restaurant sales growth of 10.9%, higher than expected, and McDonald’s (MCD) comps were even stronger at 12.6%. Price increases are fueling these comps, as restaurants seek to keep up with food inflation. But the higher prices aren’t keeping people away – McDonald’s noted that traffic rose, despite the price hikes.

Over at Procter & Gamble (PG), we learned that, on average, prices were up 10% year over year - which is incidentally much higher than the company’s input cost inflation because gross margins were up a lot. Yet much higher prices don’t seem to be hurting volumes. Similar trends were witnessed across the Consumer Packaged Goods (CPG) universe.

When first quarter earnings season first kicked off, the money center banks generally reported credit card data that shows a consumer that is still growing spending a bit, with credit card spending on Bank of America (BAC) cards, for example, up 6% in the first quarter.

Amazon (AMZN) pulled off double-digit sales growth in its oldest, most mature market, with sales in the North America segment growing 11% in the first quarter, tacking on almost $8 billion of incremental sales versus Q1 2022. No law of large numbers kicking in here… at least not yet. But Amazon is so big, it couldn’t grow this way if consumer spending in the U.S. was going off a cliff.

There are no doubt tons of headwinds to the consumer economy, including rising rates (and their impact on the cost of mortgages, car loans, and revolving debt), inflation, and the jitters that news of layoffs and bank failures can bring. But so far, we’re just not seeing a severely stressed, retreating consumer in the numbers… at least not yet.

Retail earnings season kicked off this week and has presented a few red flags. Target (TGT) saw the strength of sales weaken as the quarter went on, with February results much stronger than April’s. Discretionary goods – like home furnishings and apparel – have been weaker at Target, while sales of consumables like groceries have been bolstered by inflation-driven price increases.

Probably the most tangible sign of consumer gloom for me has been weaker results from a pair of footwear retailers over the last couple of days – Boot Barn (BOOT) and Foot Locker (FL). Usually footwear holds up better than apparel and some other discretionary categories because of a greater need for replenishment.

For some people, weakness in results at Target, these footwear retailers, and Home Depot (I’ll come back to that one in a minute) is the harbinger of a consumer-led recession that is just around the corner.

I would argue the picture is less clear. Yes, spending on discretionary goods is down. But spending on experiences is most certainly up. Looking back on that credit card data from Bank of America – people are still increasing their spending. But we have witnessed a major shift in what they are spending that money on.

Money is pouring into experiences over things, just like it did before the pandemic. Cha-ching for Delta, and even more so the hotel that its plane is taking you to…. Hilton (HLT) reported 33% topline growth for the first quarter. A few days later we saw Marriott (MAR) raise its guidance for 2023 RevPAR (Revenue Per Available Room) growth to 10%-13% from 6%-11% prior. Things are even stronger internationally – Marriott raised guidance for RevPAR growth there from 12% to 18% to a whopping 22% to 25%!

And if you’re in the Boston area this weekend, you might want to catch the Taylor Swift Eras Tour… but the cheapest ticket available on the resale sites for tomorrow – for a seat that is behind the stage - will set you back a cool $908. Helluva recession.

Don’t get me wrong – we WILL get into a recession eventually. That’s just the circle of economic life. And when that recession finally comes – and the soonest that could possibly be is the end of the year given it hasn’t happened yet – the perennial recession callers will take their victory lap, even if they have been calling for a recession since 2021.

Recession 2022. Recession 2024. Toe-mato, tah-mato.

I mock the perennial bears not because I think the timing call on a recession is easy – it’s not.

But I do want to point out that it feels like the media is almost trying to will us into a recession at this point, with constant reports of economic jitters even though 75% of the S&P 500 companies that had reported earnings had beat estimates, at least as of four days ago, when FactSet last updated this statistic.

There also seems to be a contingent that is rooting for a recession, and that crowd probably has their money – and portfolios - where their mouth is.

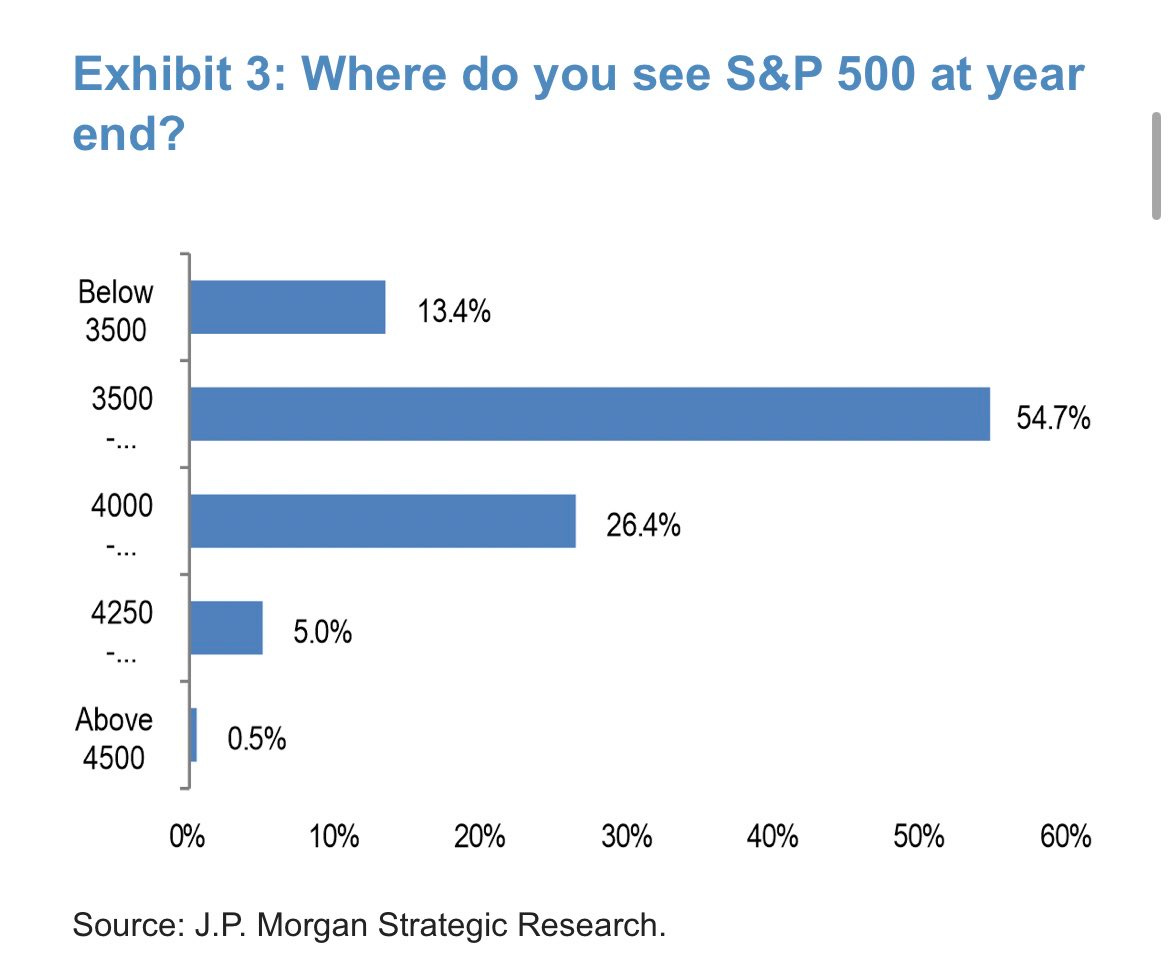

According to JPMorgan’s (JPM) latest investor survey, published in mid-April, investors are bearish:

The S&P 500 closed 4198 yesterday, so 95% of investors think we are going down from here (or up less than 2%).

I’m not a market timer nor a recession timer. But this reads very bearish to me, so if it turns out we don’t get a recession by the end of the year, many investors aren’t prepared or positioned for that, and we will probably see stocks do very well if the economy holds up, since so few people think it will.

Calling this stuff is notoriously difficult, but I will go out on a limb and predict that if we do a get a second half recession, there will be no shortage of victory laps taken. And if we don’t get a recession, there will be no shortage of people in the “just wait until next year” chorus. Which is why this, to me, is the ultimate Chicken Little recession. So many people waiting for that sky to fall….

Yes, there have been some earnings season disappointments, but there have been plenty of upside surprises too. I’ll just keep on focusing on finding the companies that can surprise to the upside. The economic environment is mixed but provides a solid enough backdrop for growth and turnaround stories that execute well to work.

Think of Home Depot as World’s Biggest Peloton Bike

The biggest whiff of retail earnings season so far belongs to home improvement icon Home Depot. When Home Depot slows down, it’s hard to ignore. This is a company that had $157 billion in sales last year. It’s the fourth biggest retailer in America – only Walmart (WMT), Amazon, and Costco (COST) are larger.

Home Depot missed consensus sales estimates by almost a billion dollars, putting up $37.3 billion in the first quarter versus expectations of $38.3 billion. Comparable store sales - or “comps” – were -4.5%, much worse than the -1.6% expected.

I would however caution against extrapolating from the Home Depot results and concluding that the consumer is dead. Falling lumber prices were a headwind to the comp. And when you dig beneath the surface of the sales contraction, you see that the decline in transactions hasn’t gotten any worse than in the last couple of quarters. The drag on sales has been ticket size, with $1000+ purchases falling more than overall sales. $1000+ purchases usually mean big home improvement projects or big-ticket items like a new fancy grill or kitchen appliance.

During the peak Covid years, people were obviously spending a lot of time at home. They not only had the money – but also the motivation and time – to deal with those projects they had been deferring until the world came to a halt. And being home more, little inconveniences that people could live with while being out and about became an in-your-face constant annoyance. It’s no secret people poured time and money into their homes during the pandemic.

That doesn’t mean that higher rates, greater economic uncertainty, or layoffs and interrupted income aren’t playing a role in a slowdown of major home improvement jobs – I am sure they are. But we also need to acknowledge that the pandemic pulled forward a lot of home investment into the 2020-2022 period. In that way, Home Depot is suffering the same fate as home exercise company Peloton, who sold at least five years’ worth of bikes in just a few quarters around the lockdowns.

The economy is clearly shifting, and the risks are numerous. But for now, I’m holding onto a glass half full versus a glass half empty approach.

And when there is an isolated data point that makes me want to panic, I just ask myself if this is truly blood in the water… or just a really, really big Peloton bike.

Tweets of the Week

I decided to add a section for some Twitter content that I found thought-provoking this week. This one got me thinking about how American-centric our definition of “franchise” is when thinking about media.

I’m not above using this space to share a tweet or two from myself. Specifically, I might want to highlight a thought that isn’t enough for a whole blog post, but might provoke some insight for people who, like me, are looking at consumer, media, and internet stocks.

I wrote this one after Disney’s (DIS) stock took a beating on earnings, just a few days after a very poorly received earnings report at Paramount (PARA):

Some Interesting Things I Read This Week

You May Never Eat Inside a Fast Food Restaurant Again

Vox, 5/5/2023

This story is about the new operating model in fast food – which increasingly features drive throughs, app pre-ordering, delivery, and no dining room. But it’s also about how our society keeps marching towards more isolation and less community. And the robots coming for jobs.

More Retail Bankruptcies Are Brewing After Bed Bath & Beyond and David’s Bridal

Forbes, 5/3/2023

Full disclosure: I am extensively quoted in this one. Spoiler: So many brick and mortar retailers on the bubble have already gone bankrupt, I think it is the dot com e-tailers that are most vulnerable to being the next wave.

MTV News Is Shutting Down After 36 Years, and Millennials and Gen X’ers are in Their Feels About It

BuzzFeed, 5/10/1023

I’m including this because I’m obviously “in my feels” about it too. I had a TV on my desk (a big fat cube one!) at my first job on the trading desk at Goldman. I remember I had it tuned to MTV when I was working late one night, and Kurt Loder came on to announce that Kurt Cobain of Nirvana had died. It was a seminal moment for Gen X. But there’s no room for nostalgia when you are burning as much cash as Paramount is. The linear to digital transition is a b*tch. There’s no mystery why Paramount is making cuts. The true mystery however is how Loder looked so young in those MTV News icon days… when he was already pushing 50!

Disney World’s costly Star Wars Galactic Starcruiser to close in late September

CNBC.com, 5/18/2023

The cost of a Disney vacation has exploded in recent years. I guess with the imminent shutdown of this immersive experience that offered Star Wars “larping” at a mere $5000 per couple for a 2-day experience, we finally have an answer to the question: How expensive is too expensive at Disney?

Did anyone make it to the Starcruiser? Who else misses when MTV was MTV? When’s the recession coming? Let me know in the comments.

Prosperous Investing!

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice or a recommendation for a particular investment.

Disclosure: The author may have a personal financial interest in the securities mentioned. At the time of publication, personal investments included MCD, BOOT, FL, and DIS.