The Earnings Miss Heard Around the World (or Capital Markets)

The Earnings Miss Heard Around the World (or Capital Markets)

Alternatively: That One Time Buying a Broken Growth Stock Actually Worked

April 20 marked the one-year anniversary of the Netflix (NFLX) earnings miss that sent the stock reeling 35% in a day, kicking off a drop that would leave NFLX shares decimated. By mid-May 2022, NFLX shares would hit a low of $166.37, completing a massive 76% drop from the November 2021 high of $691.69. Schadenfreude reigned…

Netflix lost subscribers from one quarter to the next, for the first time in memory, causing investor panic. The dream of an endless runway for growth died with that quarter, and the stock plummeted even as it started to finally turn the corner on free cash flow generation.

For years, growth investors had paid big multiples for low margins and a big cash burn because of the seemingly endless total addressable market (“TAM”). At the same time, value investors had largely eschewed NFLX shares, citing a sky-high valuation, while also critiquing a business model that failed to generate cash.

Netflix Dot Bomb

That Netflix quarter was the moment that changed everything for streaming. Growth investors’ endless tolerance for cash burn abruptly ended that day, along with their belief in the myth of a nearly infinite TAM for Netflix. Before long, layoffs would hit Netflix for the first time in memory and content budgets would get cut for the first time in its history. Suddenly, expense control mattered, as did other pedestrian financial factors like operating margin and return on investment.

Ironically, the moment when so many investors lost faith in Netflix coincided with the one that made me - and I am sure many other value investors - consider the stock for the first time.

An imminent turn into free cash flow positive territory piqued my interest in NFLX shares for the first time in years. But the thing that got me really excited was the reset in expectations. Not only had the market suddenly accepted and digested the hard truth that subscriber growth could hit a ceiling in North America, but there was a sudden rationality about the fact that margins in streaming were likely not going to match – let alone exceed – the very attractive ones that traditional media businesses had for years enjoyed within the traditional cable network ecosystem.

For those who had been filled with optimism, it was like looking into an abyss. But for many investors like me who had sat on the sidelines all these years – marveling at Netflix’s consistently impressive execution of its content and customer acquisition strategies but unwilling to get involved because both the valuation and investor expectations appeared inflated – it was a moment of opportunity.

This was of course a moment that didn’t just change everything for Netflix – it changed everything for the whole streaming industry. Since the Netflix dot bomb moment, we’ve seen cuts to content budgets, surprising series cancellations, corporate layoffs, and other forms of cost controls sweep across the streaming universe, impacting both the legacy media players as well as the upstarts.

On May 9, 2022, I made a presentation at the MoneyShow Las Vegas – an investing conference for retail investors – making the bull case for Netflix. My bull case had four main points:

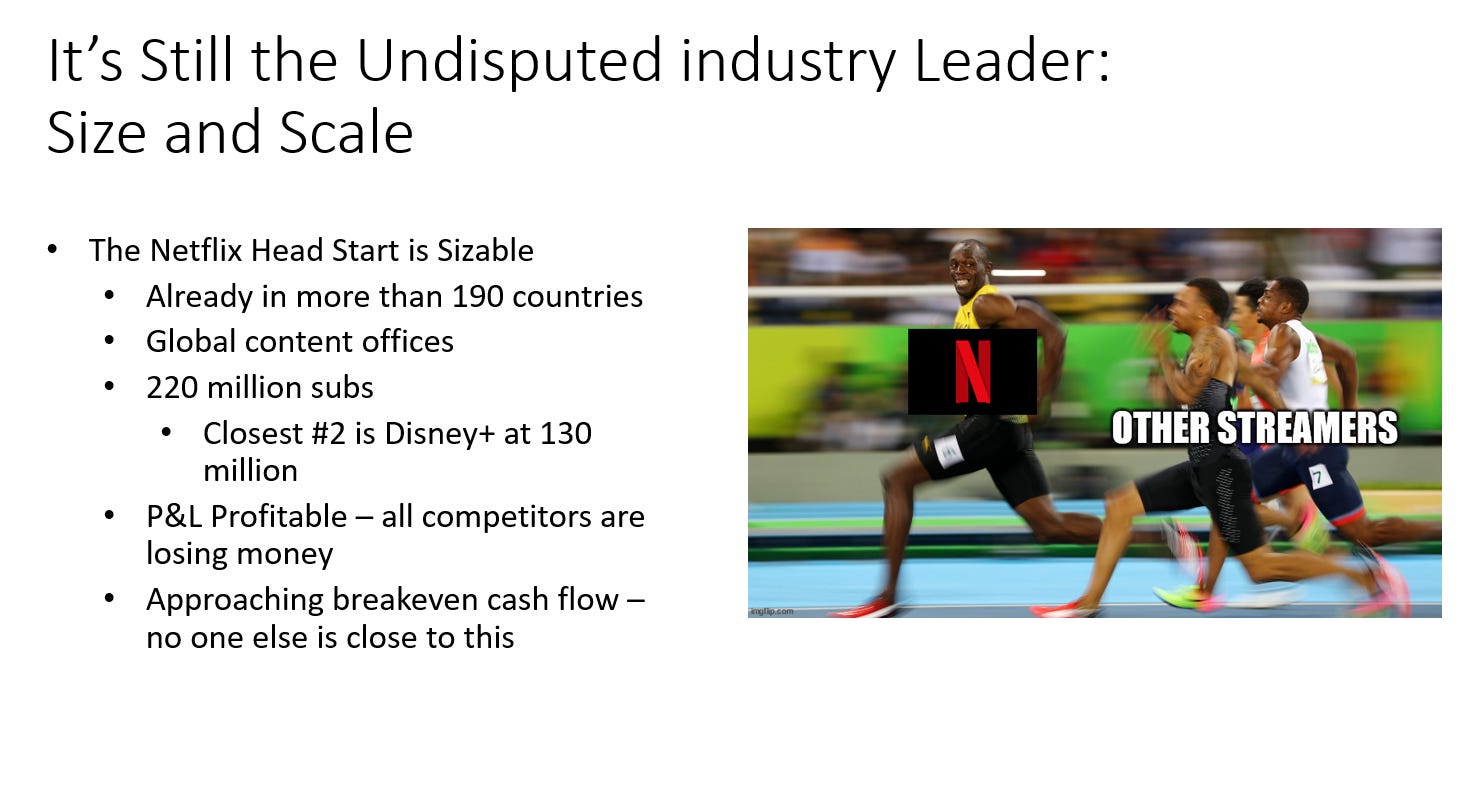

· Netflix was still the undisputed streaming leader in terms of size and global scale, and this would matter as the growth in streaming subscribers increasingly came from non-U.S., non-Western European territories.

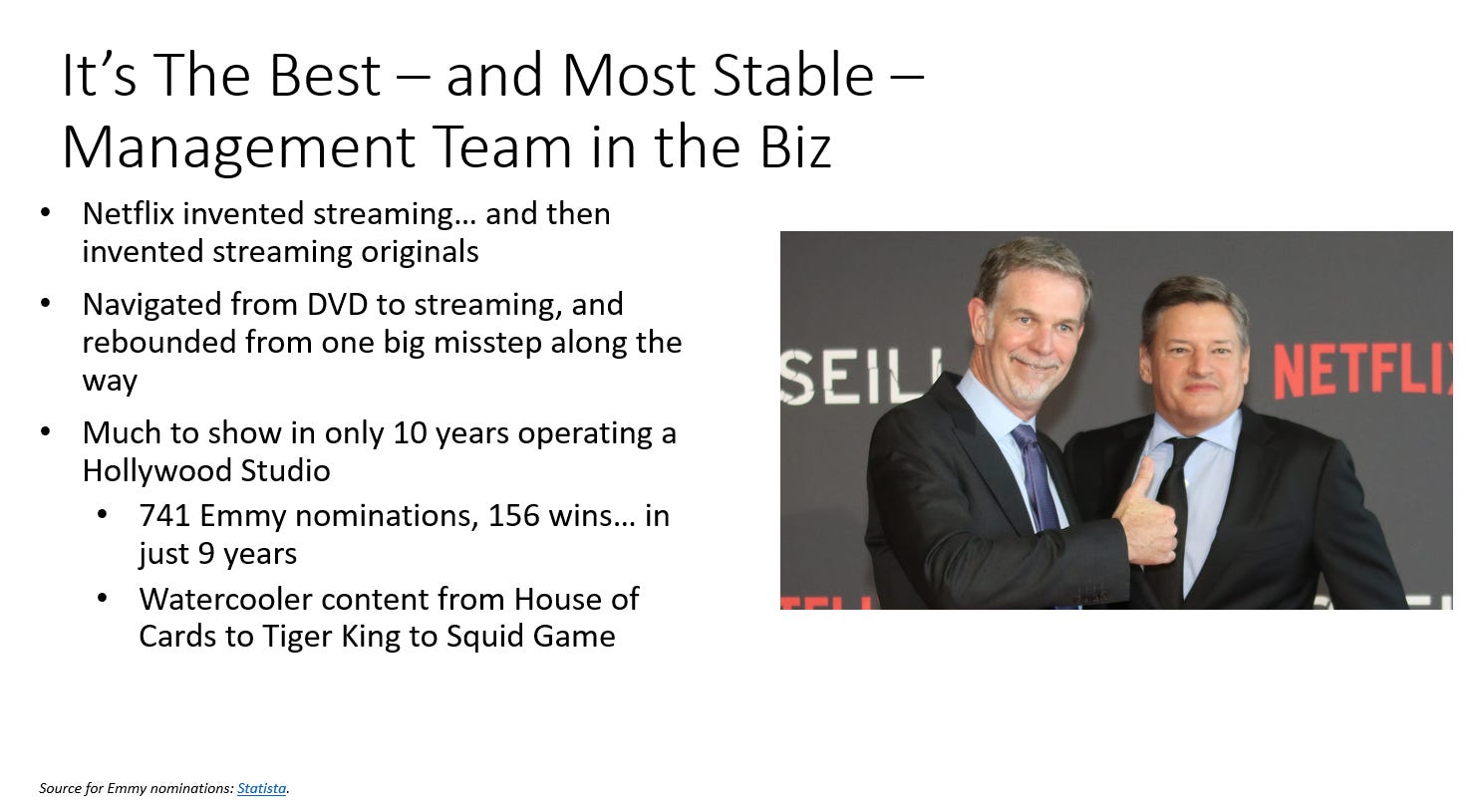

· Then Co-CEOs Reed Hastings and Ted Sarandos comprised the longest-running and best executing management team in the business – and you don’t go from hero to zero overnight in my mind from one bad quarter (Hastings has since moved to the Chairman role).

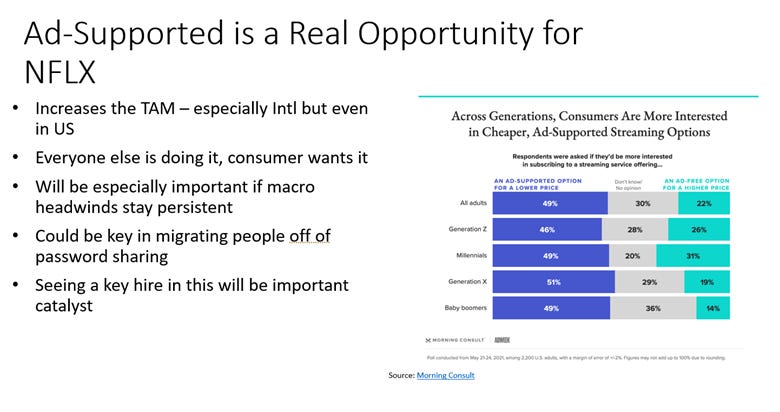

· A then newly announced lower-priced, ad-supported service represented a major growth opportunity for Netflix… and management reversing course and embracing this path that they had for so long resisted was a sign of a thoughtful, flexible, and open-minded leadership team that could change its mind when appropriate – not one that was panicking.

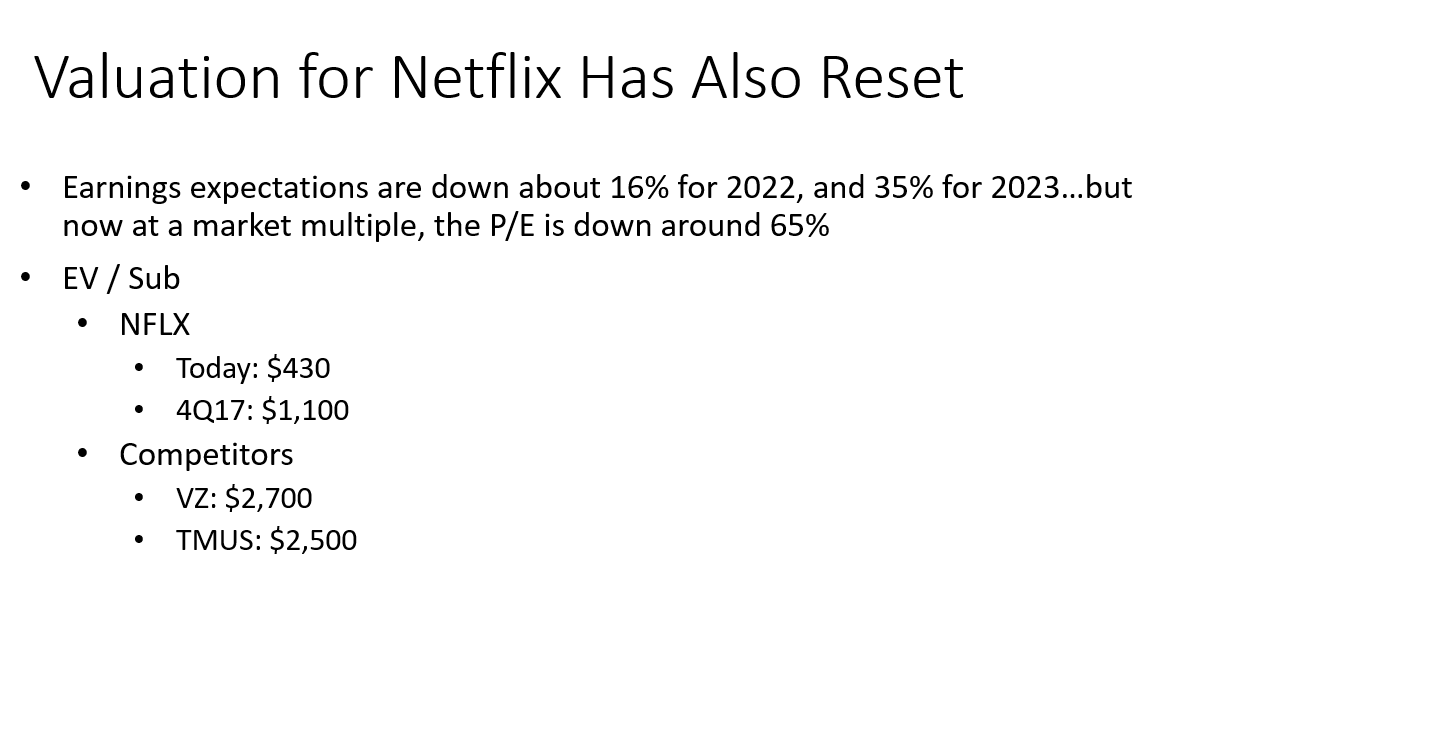

· Valuation was reasonable and investor expectations were no longer unrealistic, which de-risked the trade.

NFLX shares bottomed on May 11, 2022, two days after my presentation. Based on the 5/1/2023 closing price of $324.12, NFLX shares are up 95% in just under a year, versus the S&P 500 up just 6% in the same time period.

For the curious, here are the four slides where I laid out the bull case in May 2022 (spoiler alert: no one is giving me any prizes for my PowerPoint skills):

At the low point in sentiment, negativity was so fierce and overwhelming that the bar for what would constitute success was practically set on the floor – it just wasn’t that hard to clear it. This is why no matter how good or bad a business and its prospects are – valuation and expectations always matter. The same financial and operational results can be viewed as a triumph or a disaster based on what the expectation is going in. And the amount that a stock might rise on a beat or fall on a miss is heavily influenced by how bloated or depressed its valuation into the event might be.

I’m not going to do a full re-hash of Netflix’s recently released first quarter results, since they came out two weeks ago now… all the basics have been well-covered in the popular press, for those who care. Suffice to say, the first quarter was in-line with expectations, but the second quarter guidance was decidedly soft. Netflix did raise its full year 2023 free cash flow guidance from $3 billion to $3.5 billion, which is always something I like to see.

With the stock having nearly doubled, sentiment has obviously improved regarding Netflix – although there are plenty of vocal bears still out there. Valuation is also nowhere near as attractive as it was this time last year. Full disclosure, I had trimmed half of my position in NFLX shares during the first quarter, precisely because the set up with valuation and expectations had evolved to be more of a neutral than a positive. But the reason I didn’t sell all of my shares was my conviction in the first three bullet points, particularly the third one – the promise of potential growth from the new ad-supported plan.

The most notable data point that we got during the Netflix first quarter conference call was the statement that the new Ad-Supported Standard tier was monetizing better than the no-ad Standard Plan.

Since the Ad-Supported Standard plan in the U.S. is priced at $6.99 per month and the Standard Plan is $15.49, the implication is that Netflix is generating advertising revenue of more than $8.50 per month per Ad-Supported subscriber ($15.49 - $6.99 = $8.50). Netflix only shows 4 minutes of ads per hour, and subscribers only watch about an hour and a half per day. This implies that subscribers are generating about $0.19 of ad revenue per hour they watch, which puts Netflix slightly ahead of free ad-supported streaming television services like Tubi and Pluto… and Netflix just launched this service.

The Ad-Supported tier has limited subscribers right now, which limits the amount of ad inventory that Netflix can sell (it can only sell impressions to customers that it has). I view all these monetization numbers as promising and bullish for Netflix’s ability to monetize more price-sensitive consumers over time. Having an ad-supported tier that works greatly increases its TAM, especially internationally. And disappointment in TAM was the thing that took the bloom off the rose in the first place. I think a continued successful execution on the ad-supported front is the thing that could eventually get the growth investors back to Netflix, and it’s why I am sticking around (in smaller size) to see how the second half of this Netflix turnaround plays out.

Netflix Was the Canary in the Coal Mine

Netflix’s big tumble changed everything for the aspiring players in the streaming industry. Whereas prior to Netflix’s fall from grace, all that mattered was subscriber growth, after that moment, profits and losses took a central role.

In that way, Netflix and the streaming industry were really a leading indicator for the entire market - because by year-end, profitless prosperity would be seriously out of vogue. The idea that revenue growth can solve all business problems died on the vine. The way the professional investing community changed its tune on Netflix so suddenly and violently was a preview of what was to come for the profitless prosperity companies.

While Netflix was not profitless when that weak first quarter 2022 report sent it into a tailspin, it truly was a moment that foreshadowed the crisis of confidence that so many companies with outsized – and often unrealistic – investor expectations would face as we moved through 2022. Netflix went first, then came the small cap tech crash, the implosion of the IPO class of 2021, and the SPACs (special purpose acquisition companies – which were a major enabler of a lot of companies going public before they were truly ready for primetime).

But when excessive optimism is broadly replaced with overwhelming pessimism, there will be investment opportunities… but you have to do your homework.

Happy Tony Nomination Day, to all who celebrate.

And congratulations to the team behind the musical Parade, which received 6 nominations this morning, including ones for Best Revival of a Musical, Best Leading Actor in a Musical (Ben Platt), and Best Leading Actress in a Musical (Micaela Diamond).

This qualifies as a shameless plug because I made a small investment in this show (my first Broadway investment!). As a financial educator and guide, I have to add that investing in Broadway shows (or independent movies) is 9 times out of 10 (or more!) going to be a terrible idea! Do not do anything like this with money that you can’t afford to lose. I did it for love of the music and because I thought the story was important – not to make money. I have battered retail and media stocks to go sifting through to make money 😊

If you are going to be in New York City this spring or summer, I highly recommend you go see Parade, which tells the story of Leo and Lucille Frank. Leo Frank was a Jewish man falsely accused of pedophilia and murder in the early 20th century. As depressing as the story is, it is also a beautiful love story, with even more beautiful music, sung by a terrific and talented cast.

This is a wonderful show about “Important Things” so I encourage you to go see it, if you can. Click here to see Ben and Micaela perform and talk about the production on the Today show.

Some Interesting Things I Read This Week

I read less last week than usual because I spent the first part of the week under the weather and then spent a fun-filled three-day weekend celebrating a friend’s birthday in Miami. Incidentally, both LaGuardia and Fort Lauderdale airports were packed, and every hotel, restaurant, and night spot we visited in Miami was jammed and printing money. Hotel rates were at least twice what they were on my last visit to the city, which was shortly before the pandemic. It’s all anecdotal, but no aspect of this trip – or my trips to Houston and Jamaica in April – gave recession vibes.

Strike Watch: Reality TV to the Rescue? Not So Fast

The Ankler, 5/1/2023

Last night, the Writer’s Guild of America voted to strike, which will bring production of TV and film to a halt imminently. The last time this happened, in 2007-2008, it led to an explosion in reality TV programming. Things may play out differently this time, thanks to factors discussed in this article. As an aside, separate from the article, an extended strike would probably lead Netflix and other studios to raise free cash flow guidance for 2023, as a production shutdown temporarily lowers expenses – a phenomenon we saw play out during the COVID lockdowns of 2020.

Ecommerce, private label fails led to Bed Bath & Beyond bankruptcy

The Current, 4/27/2023

This was a very comprehensive postmortem on the factors that led this once-leading retailer to wind up in bankruptcy. You will find some quotes from me in this one.

Prosperous investing!

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice or a recommendation for a particular investment.

Disclosure: The author may have a personal financial interest in the securities mentioned. At the time of publication, personal investments included NFLX.