(Re)Introducing Consumer/Culture/Commerce

(Re)Introducing Consumer/Culture/Commerce

The more specific you are, the more general it’ll be. -Diane Arbus

I’m back after a brief hiatus, during which I spent some time thinking about what I want this blog to be. Or, more accurately, how I want to present it to the world. Everything that I wrote about in my introductory post still holds true. I’m not changing the topics I will write about nor the format, and I am certainly not changing my investing style (it’s a little late for that). But I did want to choose a name that more accurately reflects what these musings are about.

The First C

Consumer. The word can describe a sector – or two of them. There’s consumer discretionary, which encompasses retailers, apparel and footwear, gaming, lodging and leisure, consumer durable goods like furniture and appliances, media and entertainment, restaurants, luxury goods, and autos. It’s basically everything that is bought to satisfy wants as opposed to needs. Then there’s also consumer staples – the stuff you buy because you need it – food and beverages, personal care items like toothpaste, cleaning supplies, etc.

So those are the consumer sectors. But the reach of the consumer goes deeper into the economy than just those two sectors.

Per the Oxford Dictionary, a consumer is “a person who purchases goods and services for personal use.” Most of what we buy frequently as consumers is included in those consumer discretionary and consumer staples sector buckets – but certainly not everything….

We buy houses or rent apartments, but real estate is a subsector within financials. We make decisions about our health that increasingly lead to personal expenditures – either because we opt for services that are elective (Botox, anyone?) or because, sadly, critical medications aren’t on the formulary for our insurer.

How people prioritize and allocate their hard-earned money is constantly shifting. When making long-term investments, you want to understand not only where consumers’ heads are at in the moment, but also where their hopes, dreams, and perceptions are going

Even sectors that are very much business-to-business are ultimately influenced by consumer behavior. If there is migration from north to south, then commercial real estate owners of office buildings in the north may suffer. If as a population, enough individuals decide they are increasingly concerned with climate change and buy electronic vehicles or opt for public transportation, that could affect energy companies.

And this is where we get to the second C, culture.

The Second C

Why is culture so important?

Because change often happens slowly, until it finally happens quickly.

For an example, just look at the media sector….

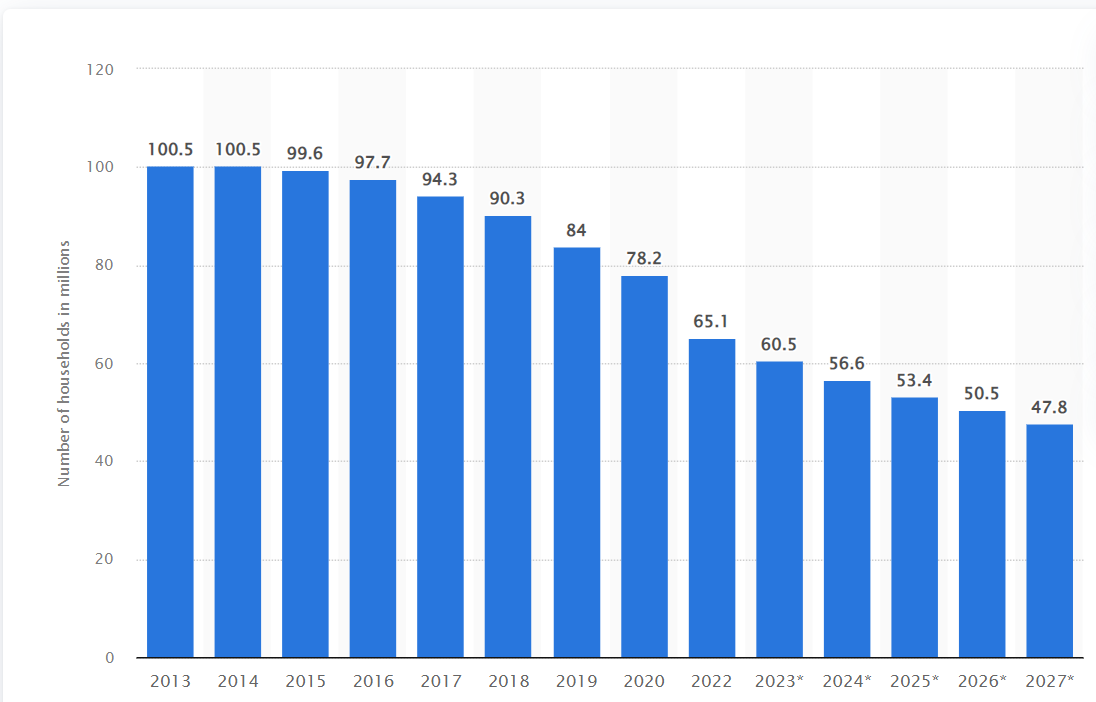

It’s hard to believe, but last January, the Netflix (NFLX) streaming service turned 15 years old. It launched in 2007, but it wasn’t until 2012 that Netflix presented its first original show, Lilyhammer. Netflix didn’t have its first bona fide hit until the next year, when House of Cards premiered in 2013. With that first hit, the first concerns about television viewing migrating from linear channels (traditional broadcast and cable) to streaming surfaced. But investors and industry pundits wouldn’t really start worrying about cord cutting in earnest until around 2016 or 2017. Meanwhile, the number of people actually cord cutting stayed in the low single digits until 2019.

Number of Pay TV Households in the U.S. from 2013 to 2027

(in millions)

Starting around 2016, cord cutting had been a major discussion topic in every meeting that I attended with cable operators like Comcast (CMCSA) and media companies like Disney (DIS). But it wasn’t until 2019 that more than a few percent of households quit cable or satellite every year. For a long time, the cord cutting trend was in slow burn and mainly a theoretical problem. But then, suddenly, things started changing more quickly.

2022 was a disastrous year for companies impacted by cord cutting, with the number of households paying for cable or satellite TV dropping by a whopping 17%, an incredible uptick from the 3%-4% attrition levels seen just a few years earlier.

Not surprisingly, 2022 was also a rather disastrous year for the stocks of companies that own broadcast or cable networks, which have historically been very lucrative.

2022 Stock Performance of AMC Networks, Comcast, Disney, and Paramount versus the S&P 500

The migration to streaming and away from linear TV is far from an isolated example of a cultural phenomenon having a large impact on stocks. There are mega-social trends all around us that influence stock movements – from eco-consciousness and electric cars, to healthy, active aging, to the casualization of dressing and the rise of remote work.

And sometimes smaller trends can be enough to move smaller cap stocks – as an example, I would point you to the story I told in my inaugural post about Lionsgate Entertainment (LGF/A). Another example of a stock-moving microtrend was the once-in-a-lifetime customer recruiting event that online crafts marketplace Etsy (ETSY) experienced when it was one of the only places to buy a mask during the early pandemic lockdown days.

I learned my lesson about how important these big cultural trends can be early in my career…. In my first buyside job, at deep value investment shop Sanford Bernstein, I was told to go chase down Kodak as an investment idea. The firm applied a dividend discount model to determine the cheapest stocks in the S&P 500, and then it would use analysts to try to either validate the investment opportunity or make a case for why the model should be overridden because the stock was a value trap.

At the time of my deep dive, Kodak (KODK) had leading positions globally in consumer film and in X-ray film and was even more dominant in the entertainment film that movies were printed and distributed on.

The model was screaming for us to buy this Kodak stock, and it was a hugely uphill climb for me to persuade the head of the firm not to. The crux of my value trap thesis was that the consumer film business was going to be toast within a decade or two. Digital cameras were already out at that time, but what I was really worried about were mobile phones with cameras in them, the first of which had just come out in Japan. iPhones, these were not. These were basic flip phones with 100,000 pixel cameras on them, and it was super hard to get the pictures off the phones and share them. Yet the Japanese were already going nuts with taking pictures on their phones.

When I presented this argument, there was a lot of internal skepticism that Americans would ever take pictures with their phones. It was like a sci-fi idea. But I managed to convince the powers that be that more of the world taking pictures with their phone was a real tail risk – an unlikely event, but one that would be catastrophic to Kodak if it actually happened. I’m sure my bosses thought I was an impractical, tech-obsessed 20-something at the time.

I don’t think I need to tell you what happened with cameras on phones and Americans, but I will remind you that Kodak, a stalwart of American business for over 100 years, went bankrupt just over a decade later, in 2012.

As for impractical 20-somethings, a few years later, I would be a stodgier 30-something when my analyst, a few years out of college, would badger me because she had seen the future in her newly released iPod Shuffle, which she was continuously plugged into, listening to tunes as she modeled away in Excel. That was the first time I ever bought Apple (AAPL) shares. Obviously, I wish I still had those shares (they were around $1 then, adjusted for splits). My future-seeing analyst is now a partner at a multi-billion-dollar hedge fund.

Then and now, seeing where the culture is going – what the things are that evoke excitement, passion, and dollars out of the general populace is a great way to find long-term winners. Which brings me to the runner-up title I had for rebranding this newsletter: The Zeitgeist.

The Oxford Dictionary defines zeitgeist as “the defining spirit or mood of a particular piece of history as shown by the ideas and beliefs of the time.”

The Zeitgeist is too obscure of a concept to use as a newsletter title, but it’s a concept that you should try to embrace as an input in your investing.

Predicting the future is often hard, and sometimes you are going to be wrong – but that’s always the case in investing. But sometimes the trajectory of the cultural zeitgeist is extraordinarily clear, and those moments usually offer exceptional investment opportunities for those willing to take a patient, long-term position rooted in their cultural point of view.

The Third C

Finally, we get to commerce, which is the exchange of goods and services between multiple entities.

I threw that in there not only because of alliteration and the fact that having three words instead of two is catchy, but also to remind people that even if you can figure out the direction the consumer is going in and how the prevailing culture is reinforcing that move, that won’t always be enough for a successful investment. There must be a viable business providing a way to play it. A strong trend isn’t enough on its own – there has to be a way to commercialize it.

Sometimes the consumer and cultural zeitgeist is crystal clear, but there isn’t a way to invest in it in the public markets. For example… between the November presale Ticketmaster crash to the absolute takeover of TikTok by Eras Tour videos, it’s clear that Taylor Swift has become an unparalleled force in American culture and is driving a lot of consumers to dispense a lot of dollars. Sadly, there is no way that I can think of to invest in that truth, at least not in the public markets.

Other times you may find a trend that public companies have exposure to, but no company has enough exposure to it for it to be needle moving. Neon clothes are a huge fashion trend now, and something most young women don’t already have in their closet.

Those items are going to move at stores this year, but no retailer is going to be deep enough in this trend for strong sales to really make a meaningful difference in their bottom-line. And if there was such a retailer– you certainly wouldn’t want to be invested in that, because as it was in the 80s, the zeitgeist will only pause on neon for so long. It’s more of a fad than a sustainable trend. A phone in your camera kind of idea, this is not!

Closing Thoughts on the Three Cs

The first two Cs are about identifying possible investment ideas, but the final C isn’t as much about idea generation as it is about eliminating bad investment vehicles for good concepts.

If you follow the evolution of consumer hopes, dreams, and desires - and how the culture is reinforcing or supporting this evolution - you will have a great chance at finding stocks with long runways for growth because of societal shifts. But once you identify the big ideas, you need to express your belief in them the right way… make sure you aren’t buying a tail that is trying to wag a dog, or a stock promotion that selling itself based on a well-recognized trend without meaningfully participating in the trend (am seeing a lot of these in AI right now!).

Some Interesting Things I Read This Week

This Rally Is All About a Few Star Stocks – and Some Investors Are Worried

Wall Street Journal, 6/6/2023

There’s probably nothing here that you haven’t heard before, but the statistics and charts sum it up nicely: the market breadth is not great and Big Tech is back, baby. At the time of the article, the S&P 500 was up 12% year-to-date, but the index if equally weighted across all stocks was up less than 2%. The disparity is due to the outsized gains of of the largest tech companies this year. Due to those gains, Alphabet (GOOGL), Amazon (AMZN), Apple, Meta (META), Netflix, Tesla (TSLA), and Nvidia (NVDA) now make up 30% of the S&P 500’s market capitalization, up from 22% at the beginning of the year. Something to keep an eye on, for sure.

Variety, 6/1/2023

If you’ve read the title, you’ve got the most important part of the story. The interesting thing is the news itself, as opposed to the article. It’s a fascinating event because Netflix management would not have lost a shareholder vote just because individual investors were sympathetic to striking writers. This vote couldn’t have been lost by management without big institutional investors taking the side of the writers, aka labor, over that of management –institutional investors like Capital Group, BlackRock, Fidelity, T Rowe Price. The WGA somehow got enough of these big investors on their side. It’s surprising they sided with labor. It could be a sign of a shifting zeitgeist, or it could be a sign these companies also manage a lot of pension money for trade unions and don’t want to alienate them. I’m honestly not sure yet which one is the truth (or maybe it’s a little of both).

The Atlantic, 6/2/2023

This article was the reported catalyst, or perhaps better to say the final straw, for yesterday’s firing of CNN’s CEO, Chris Licht, along with two of his top communications lieutenants. I guess there is such a thing as bad PR.

Here’s the real reason Target’s stock is dropping

CNN.com, 6/2/2023

Speaking of CNN, I spoke to them last week about why Target’s (TGT) stock is down. TLDR: it’s not because of rainbow merch.

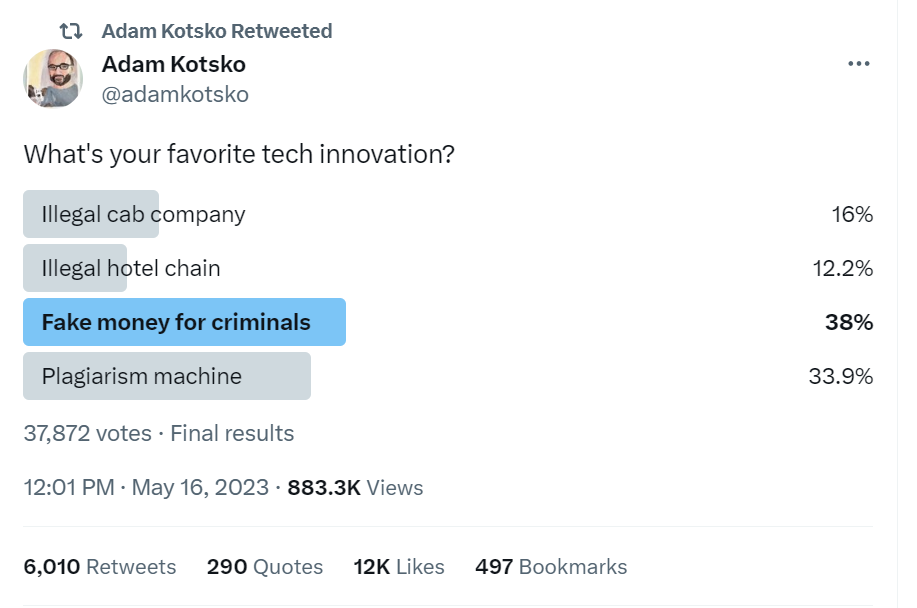

Funny Tweet of the Week

This tweet pokes good fun at some market-favorite disruptors like Uber (UBER), Airbnb (ABNB), Cryptocurrency, and AI. You can see I voted for crypto, which won by a hair.

For the record, I was voting on what was funniest. My favorite/most used of the group would be Airbnb and my pick for being the most truly disruptive (and terrifying) would be AI. I am an admitted crypto luddite.

Prosperous Investing!

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice or a recommendation for a particular investment.

Disclosure: The author may have a personal financial interest in the securities mentioned. At the time of publication, personal investments included NFLX, DIS, LGF/A, AAPL, GOOGL, and META.