Playing the Pattern Recognition Game

Playing the Pattern Recognition Game

The Buyback Edition

I’m back after spending Easter week away with the fam in a sunshine-filled paradise, which is why no post that week. Even though it feels like a lifetime ago now, today’s post is inspired by a quick trip that I took the first week of April.

Institutional Investors ❤️ Buybacks

Stock buybacks. Share repurchases. Two ways of saying the same thing. You’ve heard about them ad nauseum in earnings reports and on conference calls. But have you ever thought about why institutional investors like mutual funds and hedge funds stan so hard for buybacks?

There are three big reasons investment pros love buybacks. They’re generally accretive to earnings per share (“EPS”) and they’re tax efficient. Breaking that down….

When companies can finance their buybacks through excess cash generated by the business, the reduction of shares outstanding will make EPS go up, because the company is reducing the denominator in the earnings per share (net income/shares) equation.

As an example, let’s say a company earns $100 million dollars after tax and has 100 million shares outstanding. Its earnings per share (“EPS”) would be $1 ($100 million/100 million shares). If over time, that company uses its excess cash to reduce its share count by 20% and earnings stay flat at $100 million, EPS would rise to $1.25 ($100 million/80 million shares). Assuming the stock still traded at the same multiple of earnings, the stock price should go up by 25%, just like the EPS did.

It is possible for buybacks to be dilutive, and not accretive, to EPS. If, for example, a company borrowed money at a very high interest rate to do a buyback of shares that traded at a very high P/E multiple, it’s possible that a corporate share repurchase program could be dilutive. But more often than not, repurchase programs are accretive.

Companies can also choose to return excess cash to shareholders in the form of cash dividends instead of buybacks, but that strategy isn’t as tax efficient. A dividend gets double taxed. First, the corporation pays corporate taxes on its pretax income. Then it hands over a portion of those after-tax cash earnings to investors in the form of a cash dividend. Unless the stock is held in an IRA or some other tax-exempt vehicle, the stockholder then owes taxes on those dividends, typically at a 15% or 20% rate.

The third reason that institutional investors love buybacks is because they equate them with good capital allocation.

Some businesses are just cash cows. Many cash cow businesses, however, have limited growth opportunities in the existing business. Often in a quest to keep the topline growing at any cost, CEOs and CFOs will sink money into low return on investment (“ROI”) projects that never turn out as good as the original business was… and in the worst-case scenario, prove total flops. Value investors in these low growth businesses often press for buybacks – even going so far as to launch activist campaigns seeking them – because they would rather see the EPS grow through buybacks, a form of financial engineering, than see investment in revenue growth opportunities that don’t convert well into bottom line profits. It’s a little paternalistic that investors want to rein in the C-suite’s investments and experimentation, but history proves that buybacks almost always provide better returns for shareholders than new business Hail Marys.

Some businesses that have tremendous growth prospects also produce tremendous amounts of cash, more cash than they can invest productively, even with lots of room for growth. So over the years, the buyback evolved from being a technique primarily employed by the CFOs of sleepy value companies into one often used by cash-rich growth companies as well. Last year, Alphabet (GOOGL) authorized a $70 billion share repurchase program and Apple (AAPL) authorized a $90 billion one.

But big buyback programs don’t universally correlate with a stock being a good buy. There are plenty of companies that are notorious for repurchasing stock when it’s high and retreating when it’s low. Just like people, companies can be terrible market timers.

There are also companies that issue such an egregious amount of stock-based compensation – which of course they back out of the Adjusted EPS numbers they emphasize – that they really aren’t returning much cash at all to shareholders, just blunting the effect of their continued excessive dilution.

Even worse, there are companies with real business problems who try to use outsized buyback programs to signal their often misplaced or disingenuous confidence in future prospects. A recent example of this would be retailer Bed Bath and Beyond (BBBY), which announced an aggressive $675 million share repurchase program in 2020. Back then its market cap was only around $2.5 billion, so the program represented an intention to reduce its shares outstanding by more than 25%, using the then-current price.

Usually, companies announce buyback programs when business is good, or at least stable. Bed Bath & Beyond, however, announced its program at the start of a turnaround, with no evidence in hand that the turnaround would work. Despite deteriorating results from its core business, Bed Bath & Beyond kept raising the amount of its buyback program in 2020 and 2021, and accelerating its stock purchases, buying shares faster than it initially said it would.

Despite poor business fundamentals, the splashy buyback program was enough to sucker in plenty of investors (although I can’t think of any retail specialists I know who fell for that trick). Despite a few meme runs along the way, BBBY shares traded hands under $0.30 on Friday. Between the time I started writing this and the time I finished editing it, Bed Bath & Beyond filed for bankruptcy. Did the buyback program cause the Chapter 11 filing? Probably not. Did it hasten its filing? Definitively yes.

A basic rule of stock repurchases is you can’t buy back stock with earnings you don’t have… which explains why Bed Bath & Beyond’s big splashy buyback program turned out to be more stock marketing ploy than astute financial engineering.

Bed Bath & Beyond offers a textbook case of when a buyback program might be a red flag for a promotional management team. But in most instances, buying back stock with cash generated from operations that exceeds what can be productively invested in the business is a good idea.

One of the Buyback GOATs

I started my investing career at Sanford Bernstein, which is now part of AllianceBernstein (AB). Bernstein was, and still is, one of the most prominent institutional value investors. So, while I would say I am more of an opportunistic investor these days, early in my career, I was more of a deep value investor and ran primarily in deep value investor circles. And in the early days of my investing career, there was one stock that was almost like a cult among value investors: auto parts retailer AutoZone (AZO). Selling auto parts is a decent – but not an amazing business. And as retailers go, AutoZone was well-run but not the best run.

But what sucked in those value investors was the buybacks. So many buybacks.

In 1999, renowned hedge fund manager Eddie Lampert was riding high on great returns and a stellar reputation (this was years before his involvement in Kmart and Sears… a story for another day). His fund, ESL Investments, took a giant stake in AutoZone, and actively pushed for the company to buy back shares. And buy back they did. Take a look at this chart of AZO shares outstanding from 1999 to the present….

At the beginning of 1999, AutoZone had about 150 million shares outstanding. Today, there are about 18.5 million, down approximately 88%. Over this same time period, net income at AutoZone has grown from $245 million in 1999 to $2.4 billion in the fiscal year ended August 2022. Net income is up about 10X in 23 years. But how much is the stock up? 81X!!!

AZO shares began 1999 just under $33. On April 21, 2023, they closed at $2681.41. It’s not that AutoZone’s P/E has exploded… it’s that its share count has plummeted, propping up the EPS.

That $2.4 billion in net income translated to EPS of $117 in AutoZone’s 2022 fiscal year. But if the company still had 150 million shares outstanding like it did in the beginning of 1999, its EPS would have only been $16 on that $2.4 billion of net income. AutoZone trades at a P/E of about 23x using fiscal 2022 earnings. If its earnings were just $16, the stock would trade at $368 not $2681.

But it bought those shares, which is big part of why its stock chart since 1999 looks like this….

Without a doubt, AutoZone is one of best, if not the GOAT (greatest of all time) of corporate stock buyback stories.

Which brings me to my trip to Houston at the beginning of the month. I made the trek there to attend the inaugural investor day for Academy Sports & Outdoors (ASO). Academy went public in October 2020, a time when all roadshows were virtual and in-person meetings weren’t happening. So its first investor day served as a sort of coming out party for the company.

Academy Sports & Outdoors is a regional sporting goods retailer, kind of like a Dick’s Sporting Goods (DKS), but born and bred in Texas, with a merchandise assortment that matches that. Think Dick’s… but with more hunting, fishing, and BBQ grills.

There are a lot of reasons that I like this retailer, including its uniquely broad merchandising that makes it a great one stop shopping destination for the whole family, its strong reputation in Texas and the loyalty customers in its home market have for it, and its sharp value pricing and messaging – which I think will serve it well as the economy potentially gets more difficult. I also think the company has great merchants, and that their strategy of having good/better/best pricing in all categories is the right one for the broad demographic it serves as well as for the nature of its categories. It’s convenient to be able to get a cheap fishing pole or baseball bat when you are just trying out those activities for the first time… but it’s also great to be able to upsell the new hobbyist who gets more serious about the pursuit. The company also has a great private label program. I also think Academy will be able to open a lot more stores, given they are only in 18 states currently.

But this isn’t meant to be a deep dive into all things Academy… what I wanted to tell you about today is its capital allocation, especially its buybacks.

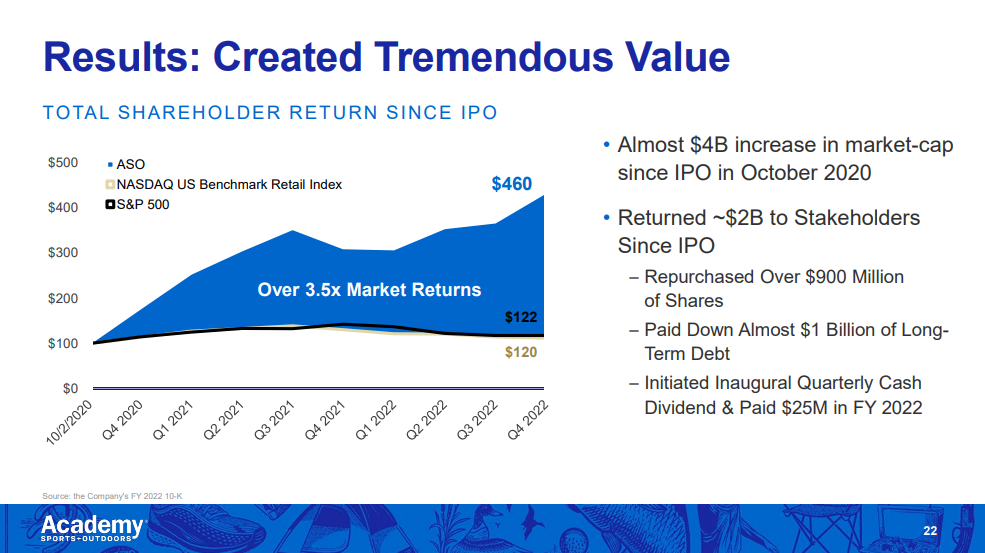

When the company went public in October 2020, it had a market cap of just $1.2 billion. Since then, the company has returned almost $2 billion in cash to stock and bondholders, including $1 billion in debt paid down, $25 million in dividends, and over $900 million in stock repurchases. Shares outstanding are down 16% in just 2.5 years as a public company.

Academy enjoyed a big jump in earnings, with net income growing from around $300 million in fiscal 2021 (the year it went public) to $630 million in fiscal 2023, which ended January 28 of this year. Part of that profit growth came from surging interest in outdoor activities during the pandemic years and some of it came from operational improvements that were years in the making. There’s a raging debate right now about the sustainability of Academy’s earnings – as well as those of competitors like Dick’s – because some investors think they are a “Covid winner” that will eventually see a reversal of fortune, as did “pandemic winners” from Peloton (PTON) to Zoom Video Communications (ZM). That skepticism is reflected in Academy’s short interest, which stands at a relatively high 15%.

In addition to impressive earnings growth, there’s no doubt that the outsized return of capital was one of the factors that propelled Academy’s stock since its IPO. ASO shares closed at $66.65 on 4/21/23 and are up over 5x from the October 2020 IPO price of $13. Academy was unsurprisingly eager to tout both its cash return as well as its stock performance at the meeting….

Academy projects that over the next 5 years, it will have approximately $3.5 billion available to return to stakeholders through buybacks, dividends, and debt paydown. For reference, that $3.5 billion is equivalent to 68% of its $5.1 billion market cap, or 65% of its Enterprise Value (“EV”), which is the sum of its market cap and debt, net of cash holdings.

This aggressive capital return plan, in conjunction with a solid operating business, prompted me to post the following tweet after the investor day….

These are probably fighting words, given AZO’s buyback GOAT status. But investing is a game of pattern recognition… If you can find something that looks like something that worked great before, it’s often worth taking a shot. And in this case, it’s not just the stock tickers that look similar.

Some Interesting Things I Read This Week

The Fox-Trump Curse & the Murdoch Kiss of Death

Puck News, 4/19/2023

Politics aside, it’s not every day that you see a company that was valued at just $80 million a few years ago receive a legal settlement that is nearly $800 million. This is the private equity windfall to end all private equity windfalls. It will be interesting to see how this lawsuit – and the ones yet to come – shape the future of television news. Good reading for those who can’t get enough of Succession. Apologies that this one is paywalled. But Puck is worth the subscription fee if you are into media, entertainment, or politics.

Outlive: The Science & Art of Longevity by Peter Attia

This is the book I started reading on vacation. I’m only about one-third through. I’m digging it, and I haven’t even gotten to the part where he tells you what habits to make so you live longer and healthier. Maybe I like it because I haven’t gotten to that part yet? We’ll see. But it’s a good read. It’s also not a very original suggestion, because it’s at the top of the bestseller charts right now.

Business Insider, 4/19/2023

I’m not even a Swiftie, but this is better due diligence than I saw from half of the Wall Street bros I know during the crypto madness of 2021-2022. SBF (Sam Bankman-Fried) … she knew he was trouble, trouble, trouble.

An Eagle Who Adopted a Rock Becomes a Real Dad

New York Times, 4/17/2023

This has nothing to do with business, investing, or living a better life. But this story made me smile all week. #TeamMurphy

Prosperous Investing!

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice or a recommendation for a particular investment.

Disclosure: The author may have a personal financial interest in the securities mentioned. At the time of publication, personal investments included GOOGL, AAPL, ASO, and BBBY (short).

Great work. I really miss your efforts at EFR.

Thanks for bringing $ASO to my attention!