My Life Is a Side Hustle

My Life Is a Side Hustle

Apparently, I’m Not Alone.

Last week, a study was published indicating that almost half of employed Americans “hold a side job or have some other form of supplemental income.” The study, conducted by consumer finance company LendingClub Corp (LC), in partnership with website Pymnts.com, found that side hustles are on the rise not only with cash-strapped, low-income workers but also with higher earners as well.

Some of this may be the economy – when inflation is rising faster than salaries, consumers can either cut back on consumption or attempt to earn more.

But a lot of the rise of the side hustle is due to structural factors and represents a generational sea change.

Internet 1.0 brought us eBay (EBAY), and with it the idea that selling used goods can be a source of extra cash. Selling used goods remains one of the most popular ways to earn money on the side, and now consumers can do it not only on eBay but also on Etsy’s (ETSY) Depop, The RealReal (REAL), Poshmark, StockX, and a long list of other sites.

In those early years, eBay was really the world’s biggest garage sale, and it wouldn’t have been possible without the internet. The internet has also made it possible for both skilled and unskilled workers to find extra hours on the side, with no shortage of apps and websites offering ways to work on demand. The best known of these gig job providers are ride hailing apps like Uber (UBER) and Lyft (LYFT) as well as food delivery companies like DoorDash (DASH), again Uber, and Instacart.

Workers with specific expertise – like digital marketing, language translation, and graphic design – can turn to freelance project marketplaces like Fiverr (FVRR) or Upwork (UPWK), and those skilled with their hands might find work on TaskRabbit. If you like working with dogs, Wag! (PET) can help you find ways to earn cash walking pups in your free time, and if you prefer to babysit humans, Care.com can hook you up with that kind of gig.

For those with capital seeking a potentially more passive type of supplemental income stream, there’s always the possibility of buying some real estate and putting it up on Airbnb (ABNB) or Expedia’s (EXPE) VRBO.

The bottom line is finding this kind of side work was historically a matter of word of mouth, networking, and perhaps, classified ads. These days, work can be sourced much more efficiently using all these sites and apps I just listed, and a ton of ones I didn’t get around to mentioning. That’s the structural piece of this.

The generational piece of this is that the side hustle is completely normal to a digital native generation who grew up with these online labor marketplaces all around them. Working a side hustle isn’t a thing of shame, it’s a point of pride.

A corporate world practically defined by a cycle of restructurings and downsizings has left work tenures shorter and eroded employee loyalty. Workers often dream that the side hustle income will eventually eclipse the salary of the 9-to-5 job, allowing workers to go full-time on the side hustle.

This makes sense because a lot of people pursue side hustles in disciplines that they are passionate about. While the number of people dreaming about driving Uber full-time is probably limited, there are plenty of people earning some cash on the side doing something they love, like selling jewelry or crafts on Etsy, making music, writing, doing photography, etc. Fashion lovers can become fashion resellers. Aspiring interior designers can become hoteliers on Airbnb. Anyone who is truly passionate about any subject – sports, entertainment, parenting, fashion, home décor, politics, finance, etc. – can aim to be a professional influencer, something that wasn’t even a career until 10-15 years ago. It’s a career only possible because of social media.

The structural changes in the way people approach work are real, and it’s a trend that’s been in place as long as the internet has been a thing. The pandemic only accelerated this side hustle trend, as working from home made it a lot easier for people to pursue these kinds of supplemental income streams. And while many people have returned to the office, a lot of people still spend at least some time at home, and schedules and physical location are just a lot more flexible for many people than they were prior to 2020, all of which is conducive to the hustle. Given these factors, it’s not really a surprise that more and more people – even ones with good salaries – have a side hustle.

The world of work is certainly a very different place than when I began my professional career in the 90s. I am pretty sure having a side hustle would have gotten me fired during my first job at Goldman Sachs. These days, when people ask me what I do, I answer by reading a list. For the record, I research companies and I invest my own money (I treat this like a job!). I also research companies for institutional investors on a contract basis – as mercenary as an Uber driver, but with a better hourly rate. I write this Substack, which at some point will layer on a premium research component with actionable investment ideas. I also write articles on investing for Public, the trading app. Finally, it’s an anomaly, but when preparing my taxes this year I actually had to report some income from gambling, which puts me in good company – apparently 4% of respondents to the LendingClub/Pymnts survey claimed betting or gambling as a side hustle.

Check back with me in a few weeks, by then there could be another item on the list of what I do for work. It’s a brave new world of work out there, and most of us on the wrong side of 35 are just trying to keep up with the times.

Tough Times at One of the OG Side Hustle Companies

Last week, Lyft co-founders, CEO Logan Green and President John Zimmer, announced they would leave their jobs by the middle of April. Amazon (AMZN) alum David Risher is joining as the new CEO.

Lyft went public back in 2019 at $72, but that price is as much of a distant memory as the pink mustaches that its drivers used to stick on their cars from the company’s founding in 2012 until 2016. LYFT shares closed today at just $9.43. So it seems things aren’t going so great.

Lyft is a poster child for what I have always called profitless prosperity. It’s a catchall phrase I use for companies that exhibit enviable topline revenue growth but fail to convert any of those revenues into actual profits.

Lyft has never made any money. In fact, last year, it lost over $1 billion. That’s a marked improvement from the $2.3 billion it lost in 2019, the year of its IPO. But it’s also a -30% net margin on its $4.1 billion in sales last year. Meh, I pass.

The argument for these companies that don’t make money and have never made money usually has something to do with Total Addressable Market, or “TAM”, if you want to sound like a venture capitalist (or just a condescending growth investor with an MBA).

The argument for these publicly traded, high revenue growth companies with no history of profitability always goes something like this: “huge TAM, land grab, make money later.” This is the rote excuse for selling things that cost $20 to make for just $15. Hook the customer, dominate the space, you can raise prices later. And you will scale against your overhead costs and IT spending better later when you are larger. Profits will explode.

But how much bigger do you need to be? Uber had $32 billion in sales last year. It still lost almost $3 billion. How much bigger is big enough?

So many professional, and amateur, investors have exhibited endless tolerance and patience for holding this type of money-burning company. I blame the infatuation with these profitless prosperity companies on Amazon….

Amazon ran in the red for years and years after its founding and its IPO. Investors who showed patience for the red ink were ultimately rewarded – it’s one of the most valuable companies in the world now. If you held on during the years of red ink, you eventually got PAID.

The 21st Century Amazon investing experience has led to a generation of investors being way too patient in my opinion with profitless prosperity, granting way too many mulligans to companies that have flawed business models. Sure, it’s easy to grow revenues when you sell a product or service for less than it costs to produce it. But when you try to raise the price to cost plus a profit, often consumers won’t see the price-value relationship anymore.

The thing that is so funny to me about everyone chasing the repeat Amazon dream, hoping that profitless prosperity will transform into a trillion-dollar market cap yet again, is that the success of the AMZN stock price has very little to do, in my opinion, with the once loss-making e-commerce business turning wildly profitable. It has everything to do with Amazon starting a new business that turned out to be wildly profitable: AWS (Amazon Web Services).

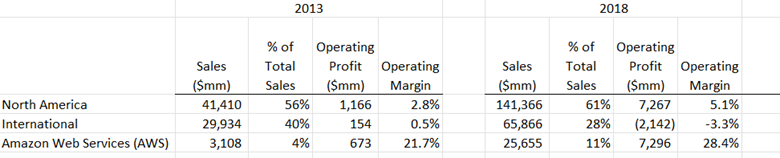

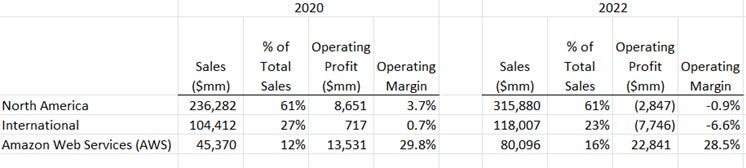

Let’s look at how Amazon made its money 10 years ago, 5 years ago, in the “peak pandemic” lockdown year of 2020, and then last year, 2022.

Looking at these financial results, a few things are clear:

· Amazon has done an extraordinary job growing its revenue in all three of its segments.

· AWS is an incredibly profitable business – it had amazing margins from the get go – which went higher with size and scale.

· The North American business, which is dominated by eCommerce - but also has other things in it like Amazon Prime Video, Whole Foods, and a very profitable advertising business - has been a low margin business from the start, and even after revenues in this business went up 7.5x, it’s still a relatively unprofitable, low margin business. Amazon is a surefire category killer in eCommerce – but the operating leverage never came the way people imagined it might 10 or 15 years ago.

· Amazon’s eCommerce businesses can earn more when conditions are great, like in 2020 – eCommerce did fantastic during lockdowns. That business will earn less – and can even go negative – when the sector and macro environment get worse, as it did in 2022 with inflation, inventory gluts, and a more promotional retail environment.

· The International business, again, dominated by retail, was barely profitable even in the best year in the history of time to be an e-tailer, 2020.

Don’t get me wrong – what Amazon has done in e-commerce is jaw-dropping. It has changed the way we live. Amazon transactions generally fulfill the goal that the company set out to do way in the beginning, “surprise and delight” the customer. I have Amazon boxes come to my home several times a week. You probably do too. I shop for categories on Amazon now that I never would have thought I would 10 years ago, such as fashion. They have done an incredible job.

But if there were no AWS, there would be no trillion-dollar valuation. Even granting an incredibly generous valuation of 30x operating income for a single-digit-operating margin business and applying that to peak non-AWS operating profits from 2020, you would get a $300 billion company, not a $1 trillion one. And this is with being generous with the valuation multiple. AWS has been the driver of the astounding rise in AMZN shares, not the eCommerce business, which has been incredible in terms of revenue growth, but not margin expansion.

Getting to double-digit operating margins in the non-AWS business at Amazon – something that was contemplated all the time 10 or 15 years ago - still hasn’t happened, even with sales north of $400 billion.

So unless you think Lyft is going to stumble into an AI business (like Amazon did with cloud computing) - or some other high growth business with structurally higher margins - I would stop the “wait until next year” approach to this profitless prosperity company. The track record of consumer technology companies that have lost money suddenly sustainably going into the black? It’s a short list. Congratulations to Netflix (NFLX) and a few others for pulling it off… but that doesn’t mean you should be holding your breath for lightening to strike at Lyft.

2023 is of course the year that Wall Street analysts expect Lyft to finally turn profitable. I’ll believe it when I see it.

Profitless prosperity was super in vogue in late 2020 and 2021. People wanted to believe in the dream.

Somewhere in 2022, a preference for dreaming was replaced with a pragmatic eye on bottom-line profits. This shift in investor preference is why streaming companies are no longer judged primarily on subscriber growth but on progress towards profitability. It’s why there are a ton of companies that went public via a SPAC (special purpose acquisition company) – without a profitable business model – are down 80% or more now.

Profitless prosperity is so 2021. Don’t fight the last market’s war.

Some Interesting Things I Read This Week

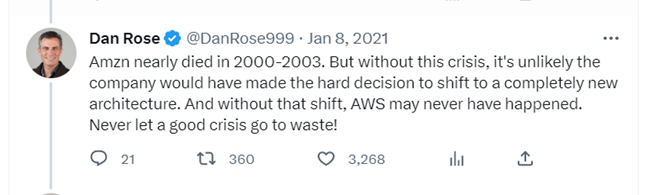

A brief Twitter thread by an Amazon alum on how the company stumbled upon the completely transformative AWS business. From January 2021.

OK, I admit I didn’t read it this week. I read it when it came out. But I remember it vividly two years later… it was that good. And it’s a must read for anyone who wants to understand Amazon, and also the unique aspects of its history that make other companies unlikely to repeat its trajectory. Here’s a key summary tweet from the thread:

Commercial real estate is in trouble. Why you should be paying attention.

CNN.com, 3/27/2023

I’ve long thought that Mall REITs were in trouble (been short them off and on since 2017) and since the pandemic, I’ve been negative on Office REITs (and short two of them). These are obvious trades – the way that we shop and work has been radically altered. As obvious as this statement about behavioral shift is, the short trade on these real estate sectors only got popular pretty recently. Now these secular concerns have met rising interest rates, and lots of people are worried about Commercial Real Estate (CRE). This article does a good job explaining the basics, and also tying the problem into the risk that CRE poses to banks, something I had admittedly spent less time thinking about until I read this.

The Conversation, 4/4/23

TL: DR – the IRS is going to get up into your Venmos in 2023. Seemed on topic for today.

Meta, Microsoft, and Disney are reversing their bets on the metaverse

Quartz, 3/30/2023

Schadenfreude of the week.

Dungeon & Dragons’ Epic Quest to Finally Make Money

Businessweek, 3/30/2023

D&D’s parent, the toy company Hasbro (HAS), is a company that I believed was quite well run for many of the years that I have followed it (which is a lot – at least 15 years). It’s recently fallen on tough times and its stock price has been cut in half. The whole toy industry is fighting tough comps, as toys were a big pandemic spending beneficiary. Margins have been under pressure. Its well-respected and gifted longtime CEO, Brian Goldner, died in 2021 at just 58. This article offers a deep dive into a strong but under-monetized asset in its portfolio: Dungeons & Dragons.

YouTube, 4/4/2023

OK, this isn’t reading. But it’s a nice compliment to the D&D long read in Businessweek. And this trailer has already inspired a wave of memes on social media. Over the last 15 or so years, Hasbro did a great job monetizing and driving its toy business by going deep into the entertainment space, through movies like the Transformers series and TV series like the one based on My Little Pony. Mattel (MAT) slept on the potential to drive its toy sales with movie franchises for years – now it is playing catch up. All eyes in Hollywood – and in the toy biz – will be on Barbie when it opens in July.

Prosperous Investing!

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice or a recommendation for a particular investment.

Disclosure: The author may have a personal financial interest in the securities mentioned. At the time of publication, personal investments included REAL, NFLX, META, and DIS.