A Very Good Week for Target and a Very Bad One for Twitter

A Very Good Week for Target and a Very Bad One for Twitter

Follow the Inventory for Retail, Maybe Don’t Follow Controversial Social Media Accounts If You are a CEO

Target Has Healed Itself…or At Least Half-Healed Itself

Last Wednesday, shares of retailer Target (TGT) jumped nearly $20, or 18%, tacking on almost $10 billion in market cap in a day in reaction to a healthy earnings beat of $2.10 per share versus expectations of $1.47 per share. There was a modest sales beat, but the real upside came from the margins, with the operating margin coming in at 5.2% versus expectations of 4.0%.

The move last week was a welcome respite for long-suffering TGT shareholders, who have been living through, along with the retailer, a very extended pandemic hangover.

The pandemic times were obviously very good for Target, as you can see in the chart above. In the early pandemic, Target was able to stay open as an essential retailer selling food, medicine, and other necessities. With most competitive retailers selling discretionary goods closed, Target temporarily became one of the only places around to buy things like clothes, toys, sporting goods, kitchen items, and electronics in person.

Once competitors were allowed to re-open, the pandemic still brought a lot of traffic to Target’s stores and website.

In the years prior to the pandemic, Target had invested a lot into both its grocery offerings and its e-commerce capabilities. Some of those improvements and investments hadn’t been fully recognized by consumers until they were scrambling for groceries during times of shortage, or they experienced temporary slowdowns in Amazon’s (AMZN) shipping times, which led them to go see what traditional brick and mortar companies like Target and rival Walmart (WMT) could do online.

As stores everywhere in all sorts of categories struggled to stay in stock during supply chain interruptions, both Target and Walmart used their scale and power over suppliers to stay in a relatively strong inventory position. It was a great time for these two companies to recruit new customers and reactivate old ones, allowing them to grab share of consumers’ wallets – at a time when those wallets were full of stimulus money ready to be spent.

By 2022, the stimulus gravy train was over, and inflation and interest rates were on the rise. And the money that people did have to spend, they suddenly wanted to spend on experiences – travel, dining out, concerts and sporting events – not on more stuff. After struggling to stay in stock for all of 2020 and 2021, Target – like almost every other retailer - found itself out over its skis on the inventory front. After chasing inventory for several quarters, Target suddenly found itself heavy on inventory at the exact same time that sales started slowing down because of the aforementioned macro factors as well as the diversion of disposable funds to buying experiences over things.

When retailers have too much inventory, there’s only one thing to do… put it on sale. Which is why you always need to follow the inventory in retail.

The Most Important Equation in Retail: Sales Growth – Inventory Growth = The Future

At its heart, the retail business is about buying the right stuff so that you can sell it for more than you paid for it. Sure, it’s important to put the store in the right place, make it the right size, hire the right number of people – not too many and not too few, and do all the other things required to operate efficiently and optimally. But if you don’t buy the right product and the right amount of it, no amount of operational efficiency will save you.

Judging the quality and appeal of inventory for any retail company – especially one as large and diversified as Target – is a difficult and extremely subjective measure. But quantity is easier to measure, which gets to this magic equation referred to in the subject header above.

Sales Growth – Inventory Growth = The Future

The idea is that when sales growth outpaces inventory growth, gross margins will probably trend positively in the near future, as the need to discount merchandise is likely to drop sequentially. When sales growth lags inventory growth, gross margins will likely fall because of the need to discount to get rid of that excess inventory.

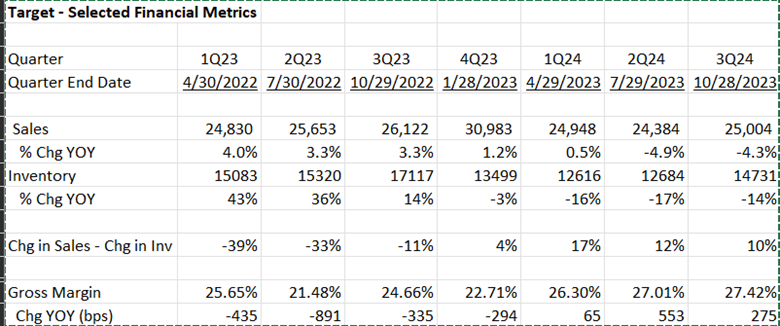

You can see this phenomenon at work for Target by looking at selected financial metrics from 2022 and 2023. Big increases in inventory that exceeded the rate of sales growth were a tell that gross margins were going to plummet, which they did in 2022, bottoming in the second quarter of calendar 2022/fiscal 2023 (remember that retailers have that pesky January year end).

Target obviously did a lot of work on their inventories with some serious clearance sales after the holidays last year, evidence of which you can see in that 3% drop in inventory by the end of the fourth quarter of fiscal year 2023. Sales were marginally positive and outpaced inventory growth that quarter for the first time in several quarters, so it’s not shocking that gross margins started improving incrementally on a year over year basis by the next quarter.

Inventory improvements accelerated in the first half of this year, as Target continued to clear through the inventory it had on hand and must have been very judicious in its ordering of new products. Even as sales weakened throughout the this year due to a variety of macro factors, the inventory drops outpaced the sales drops, setting the company up for a healthy gross margin rebound.

Probably the biggest surprise here is that the stock didn’t move up more on the giant 553 basis point improvement in gross margins witnessed in the second quarter this year. But I think that improvement was probably overshadowed by that being the quarter that sales momentum really started to slip and topline revenue growth turned negative. Tighter consumer budgeting has been a giant headwind to Target’s sales of discretionary goods, and for the half of the business that is consumable and non-discretionary – the stuff like food and toothpaste – inflation started to taper off and become a headwind to sales, after being a tailwind for several quarters.

The second quarter was also the peak of pressure on operating expenses, which were still up for Target in Q3 on a percentage of sales basis, but not up as much as they had been in Q2.

There was a lot of noise in Q2 to throw you off the scent of the improving inventory situation at Target, but if you could look through that noise, and follow the magic formula, you would have done well and enjoyed last week’s big move.

So What to Do Now If You Missed the Big Move?

The answer depends on your time frame. If you are trying to make money in weeks, months, quarters… move on, because the easy money has probably been made in Target. The company has done a lot of work fixing its inventory, optimizing its logistics and digital fulfillment costs, and addressing its problem with shrink (theft) with those incredibly annoying locked cases – which the company is trying to sell a story about customers liking!

With a lot of work done on the cost side, the focus is going to turn to sales momentum, and rebuilding that has a murky timeline, with macro headwinds out of the company’s control. While Santa may not be bringing everyone coal this Christmas, the chances of a blockbuster holiday season feel decidedly remote. It’s unclear what the next catalyst is for Target since that catalyst probably needs to be topline-related. For its shares to move significantly higher, Target probably needs same store sales to return to positive territory, and that might be several quarters away.

If, however, you are a longer-term investor with a multiyear time horizon, I think Target is interesting here. TGT shares trade around 9x EBITDA and a P/E of 16, which is an about average historical valuation for the company. But the opportunity lies in the fact that Target is still underearning at the moment, with margins below long-term averages. And I do think the company will eventually recover its margins due to its strong merchandising prowess. Remember – the job of a retailer is to buy the right product and the right amount of it. And Target has been one of the best, for a very long time, at choosing the right products.

I don’t believe Target has lost its merchandising magic – the ability to deliver great fashion in apparel and home goods at an unbeatable price. There’s nowhere else where I have consistently bought things for under $50 that draw raves from strangers on the streets of New York. Target still has that ability to surprise and delight with the elevated but affordable products that earned the company its nickname Tar-Jay. And the ability to get that great discretionary fashion and home product in front of you when you dash in to grab a gallon of milk or replace your shampoo is a great strategy, especially in the internet age.

Target sells consumables that have a sense of urgency that the internet can’t fulfill, and while they have you there, they have the opportunity to sell you something you want, but don’t really need.

I believe in buying retailers when they are out of favor, down but not broken – which is Target today.

Target has come a long way towards fixing its margins, now it needs to fix its sales momentum. I believe Target will get there, but it will take some time, so this stock is a good one only for the patient.

How to Lose $44 Billion Without Really Trying

It’s easy really… you just need to be a billionaire with poor impulse control and controversial opinions!

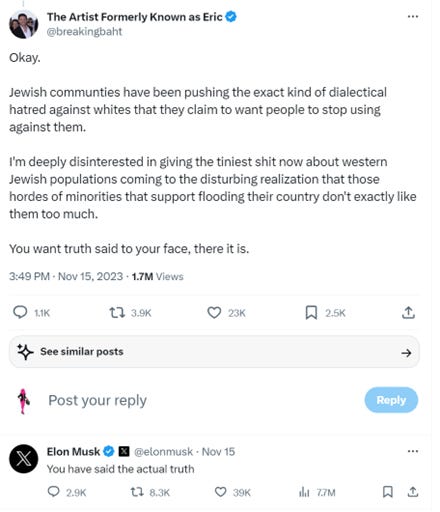

ICYMI, last week, Tesla (TSLA) and SpaceX CEO and X (aka Twitter) Chairman and owner Elon Musk set the internet on fire by commenting on and agreeing with a tweet that many perceived to be antisemitic. Here’s the tweet and Musk’s response:

I’ve heard passionate arguments for both why this tweet is antisemitic and why it isn’t. I’ll leave that discussion for elsewhere, and instead focus on the undisputed fact that many advertisers found it antisemitic enough to be toxic, and pulled their advertising off Twitter (sorry, not sorry – I just can’t call it X!).

In the wake of the controversy, companies including Apple (AAPL), Disney (DIS), IBM (IBM), Lionsgate (LGF/A), Paramount (PARA), Sony (SONY), and Warner Bros. Discovery (WBD) have suspended advertising on Twitter.

The list of advertisers who fled the service is heavy on tech and entertainment companies, which may be because they were among the few industries where leading companies hadn’t already fled the service. As of late October, the one-year anniversary of when Musk took control of Twitter in a $44 billion take private deal, ad revenue had already plunged 55%... and that is before the latest defections.

When Musk took over, he quickly cut 80% of headcount, including almost everyone at the company that was devoted to “brand safety” efforts. If you’re unfamiliar with brand safety, it’s the desire of advertisers to protect the image and reputation of the product, brand, or service being spotlighted from any damage that might result from sitting side by side inappropriate content. Inappropriate is kind of in the eye of the beholder, but generally things like nudity, sexual content, extreme violence, or racist/misogynist/bigoted text are all things that would be considered brand unsafe.

Because social media is dominated by user-generated content, platforms can’t fully control what goes up on their apps and sites. Companies like Meta (META) and Alphabet (GOOGL) have invested tons of money in trying to filter out content that might be offensive for advertisers on properties like Meta’s Facebook and Instagram and Google’s YouTube. Even with these guardrails, occasionally marketers will temporarily pull back from advertising on these platforms when they think it is a moment of heightened risk to brand safety, because no one wants to see their product ad show up next to a video containing graphic violence or next to a tweet blaring racism.

With the dismantling of brand safety efforts, many big advertisers had already left Twitter. Also, the service has been bleeding subscribers since Musk’s takeover, with monthly active users (“MAUs”) down 18% in the U.S. year over year as of September, according to data from SimilarWeb (SMWB). Twitter was already on the ropes, and Musk’s ill-received tweet may have dealt the social network a death blow, at least from an advertiser perspective – and advertising is the overwhelming majority of revenues at Twitter.

A company can’t survive indefinitely without revenue, even with one of the richest men in the world as its benefactor.

It is truly a headscratcher why Musk couldn’t keep his mouth shut… there’s only downside from treading into politically treacherous waters as a CEO. And no matter how rich you are – even if you are $240 billion rich like Musk - a potential wipeout on a $44 billion investment is not something to take lightly – you want to avoid that. So keeping quiet doesn’t seem like it would be that hard. But people don’t get to be as rich as Musk is by playing by the rules, so shifting gears to play by the rules to preserve wealth probably isn’t in his DNA either.

While the precariousness of Twitter’s financial position has almost certainly grown from this latest episode of “men behaving badly,” the bigger question for investors is what this does to Tesla, which unlike Twitter is still a public company.

I’ve made it a career policy never to trade TSLA shares nor offer investment advice regarding the stock – it’s too much of an emotional battleground for me. But if you are a Tesla investor, it’s worth giving some thought to how Musk’s antics at Twitter will ultimately impact Tesla’s brand and the demand for its cars. At best, Twitter is just a distraction for Musk, something that is redirecting his focus from his primary job – managing Tesla. At worst, it is a platform for him to alienate and drive away future EV customers.

Tweet of the Week

This gave me a good laugh.

Some Interesting Things I Read Recently

Lauren Sanchez Is Looking to the Future

Vogue, 11/13/2023

Presented without comment. There’s so much that’s been said, and so much I could say, but I will let it speak for itself.

Pew Research, 11/15/2023

32% of Americans between 18 and 29 regularly get news from TikTok. If you’ve spent any time on TikTok, you probably know that this is not good news.

Temu Is Burning Cash to Challenge Shein and Amazon on Black Friday

Wired, 11/21/2023

Temu has come virtually out of nowhere to challenge incumbent brick and mortar retailers in the U.S. as well as e-commerce giant Amazon. Temu’s barely been around in the U.S. more than a year, but it’s the #1 app today in Apple’s iOS App Store.

Prosperous Investing!

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice or a recommendation for a particular investment.

Disclosure: The author may have a personal financial interest in the securities mentioned. At the time of publication, personal investments included AAPL, DIS, and LGF/A.

Thank you for the post.

I wonder if you have a view about PLCE (and if not, totally fine).

Some good points for the attractiveness were made by presentation from David Bastian in this pitch at MCC https://www.youtube.com/watch?v=wzOuWzjhsbg. Main driver is return of high cash flows to pre-covid levels when costs normalize again. Also revenue decline was less than inventory decline in the last 2 quarters, with improving GM%.

But on the other hand: Revenue has been declining yoy for quarters, PLCE continues to close stores, and leverage is significant. While management expresses optimism based on some anticipated improvements in cost basis - their statements don't matter much, because they have to convey optimism, especially with this leverage.

I am curious whether you have a view about PLCE, e.g. how you assess the potential vs. the risk / decline, and what is not reflected in the current valuation.